Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Nach der Durchsicht von über 200 wissenschaftlichen Artikeln, die im Verlaufe der vergangenen 40 Jahre erschienen und in welchen das Wort Fintech benutzt wurde, hatte ich in diesem Artikel die folgende Definition des Begriffs Fintech abgeleitet:

“Fintech is a new financial industry that applies technology to improve financial activities” (Schueffel, 2016; p. 45)

Da der Artikel ausschließlich auf Englisch veröffentlicht wurde, erreichten mich zwischenzeitlich zahlreiche Anfragen, wie diese Definition ins Deutsche zu übersetzen sei. Gerne möchte ich diese Frage mit der folgenden deutschen Definition beantworten:

„Fintech ist eine neue Finanzindustrie, welche Technologie verwendet, um finanzielle Aktivitäten zu verbessern.“

Mit besten Grüssen

Patrick Schüffel

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg

Chemin du Musée 4

CH-1700 Fribourg

patrick.schueffel@hefr.ch www.heg-fr.ch

“Fintech is a new financial industry that applies technology to improve financial activities.” (Schueffel, 2016; p. 45)

This is the definition I derived after examining more than 200 scholarly articles that were published over a period of 40 years and which are referencing the word Fintech in one way or the other. Building on the commonalities of the definitions that found entry into those peer-reviewed journals I distilled the definition provided above.

I am proud that my work withstood the rigorous double-blind peer review process of the Journal of Innovation Management and was published these days.

As the Journal of Innovation Management is an open access journal you can retrieve the full text by using the following link:

Schueffel, P. (2016). Taming the Beast: A Scientific Definition of Fintech. Journal of Innovation Management, 4(4), 32-54.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

The number and diversity of Fintech offerings is soaring. As banking clients increasingly often enjoy not only a better user experience, but also cheaper rates at Fintech firms, their willingness to be locked-in with one or two universal banks diminishes. Henceforth clients will gradually assemble their own individual “banks”, comprising a range of offerings from different Fintech companies. Those firms which will be able to provide an overarching structure to seamlessly wrap the multitude of Fintech offerings will experience their heydays.

Modern production technology allows what would have been inconceivable only a few decades ago. If we want, we can have products of mass production tailored to our needs nowadays. Dell made only the beginning when first assembling PCs to our requests on a large scale. Today we order our tailored sneakers at Nike ID, wear a unique t-shirt from Spreadshirt and eat M&M’s sporting our very own initials. Yet, the trend of mass customization did not stop in the manufacturing sector. We can already observe its ramifications in the financial services industry where Robo-Advisors offer retail customers to tailor their client portfolios. But this is not the end point of the evolution. It is the mere beginning which will eventually lead to tailored banks.

The personal balance sheet

Like it or not, every single one of us carries his or her own very personal balance sheet: On the asset side, we have liquid asset positions such as the cash that we have in our wallets, the money on our current accounts, our savings accounts or money market instruments. Our personal investments may comprise medium term notes, bonds, stocks, mutual funds, pension savings and/or alternative Investments. Finally, we may possess highly illiquid real estate investments such as our primary residences, vacation homes or even property that we rent out.

On the liability side we may also have a variety of items. Current liabilities may include unpaid bills, credit card balances, taxes due, installment loans due in the short run, consumer loans, car loans, student loans, mortgages due within one year etc. Non-current liabilities may include any consumer, car or student loan that is due after one year. Last but not least, we may have mortgage debt for our primary residence and/or vacation homes and/or rental property.

Hence, as individual as we are as human beings, as individual are our personal balance sheets. Yet, what we do have in common is that we willingly or unwillingly manage these balance sheets. We carry out treasury functions on our personal balance sheets by paying bills and installments, transferring money from one account to another, by investing in shares or by redeeming mutual funds etc.

The Fintech Alternative

So far many consumers in the western world have ties to one or two banks, oftentimes universal banks, that cater to all of the needs resulting from these treasury transactions. Yet, the service offerings of universal banks are increasingly rivaled by Fintech firms that offer a narrow, yet highly specialized service or product.

If you have a little cash to spare, Fintech firms such as Creditgate24, LendingClub or Crowdcube, have offerings for optimizing liquid assets. To manage longer term investments one can turn to providers such Wealthfront, Moneyfarm, Nutmeg, Addepar etc. On the liability side, too, there is a vast array of Fintech companies jockeying for position. Current and medium term liabilities may be optimized by using Affirm, Borro, Lendable, Prosper etc.

In order to transfer money from one provider or account to another the consumer can chose among dozens of payment providers such as TransferWise, LiquidPay, Paypal and the likes. For trading purposes the client may want to turn to eToro or Robinhood. Even donating money becomes easier and less burdensome with Fintech providers such as Elefunds.

These new type of financial services providers that found their niches on specific links of the value chains of universal banks typically not only promise their clients a better user experience, but also lower costs. What is thus foreseeable for the near future is that clients will no longer accept to be locked-in with one or two banks, but that they will make use of a range of financial service providers. Eventually every user will assemble his or her very own bank, the IBank* as I call it.

Assembling the IBank

The IBank will comprise a selection of services provided by specific Fintech companies handpicked by the individual client. This can happen dynamically and on an ad-hoc basis or on a more permanent base. The client – or an overlaying algorithm for that matter – may decide on a case-by-case basis which payment service would be optimal for a specific transfer. On a more longer term basis one mortgage provider may be chosen until the renewal of the mortgage is due.

What is important to note, however, is that clients will make use of tailored “banks” which may be as personal as their individual balance sheet. The challenge and opportunity in this future banking world will be to provide the glue that seamlessly keeps together these services provided by different providers. Those providers who manage to assemble and maintain an overarching structure that smoothly integrates the multitude of service offering of Fintech providers will have a bright future in finance services world which is being ever more atomized.

*IBank like “I bank” – not to be mistaken with the iBank offerings by Barclays, The Bank of Georgia, Fransabank, BCU and so on.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Bundling will be the next big Fintech topic after unbundling and platformization. Just as consumers got used to buying different food items at one single supermarket long time ago, they will expect one-stop-shops for financial services. Those “bundlers” that manage to seamlessly offer cost-efficient and dynamic bundles are well poised for success in this next race in the Fintech arena. Some important lessons can be learned from previous bundling attempts, such as Deutsche Bank’s “Moneyshelf”.

In 2002 Deutsche Bank started an immensely ambitious e-commerce project. The objective of the project by the name of „Moneyshelf“ was to establish a financial super market. The goal was to create a one stop shop for virtually any financial product a retail client could wish for – across any provider existing. The underlying idea was to provide off the shelf financial products from any makers and brands. The reasoning behind it was that consumers would also frequent supermarkets to conveniently buy various products across brands and manufacturers. A modern consumer would visit a single supermarket to purchase bread, sausages, apples, beverages, canned food and cleaning liquid. He or she would no longer go through the ordeal of visiting a bakery to buy bread, a butcher to shop for sausages, a local market to get some apples and then drop by yet another store to buy beverages and food before visiting the local drug store to buy cleaning liquid.

Creating a financial supermarket

In order to use such a financial supermarket the client was requested to deposit his access information to any other banking service with the Moneyshelf platform. Moneyshelf would then let the client consolidate and manage all of his or her accounts in one highly user-friendly frontend. In the background online banking interfaces programmed by Deutsche Bank developers would ensure the interoperability. Moneyshelf promised a quantum leap in transparency and price efficiency. A client who would have a securities account with bank A and be invested in mutual funds from fund provider B could then not only shop for a more cost-efficient securities account, but also a better performing and less costly mutual fund und would only be a mouse click away. All of this was paired with features such as personal financial planners which offered insights on the clients’ spending and financial behavior and a rich offering of financial information and possibilities of analysis.

Deutsche Bank ahead of times

Moneyshelf as it was envisioned by Deutsche Bank was offering the client a tremendously versatile platform to choose among a vast range of providers and products such as current and savings accounts, mutual funds, brokerage services, mortgages, even life insurances. Deutsche Bank sensed that clients would become more tech savvy and consider the threat to be very real that Deutsche Bank may soon be disintermediated as far as their retail segment was concerned. With the emergence of online brokers and their strong growth Deutsche Bank feared of getting skinned and decided to take the bull by the horns. Hence, should a client decide to do business with a different bank, then Deutsche Bank would make sure that it would at least get a share of those revenue streams bypassing them.

The bone of contention: depositing client data

In the end this business model failed big time. The other banks, especially the rather dominant German savings banks warned their clients that it would be a violation of their contractual obligations to deposit account access information with any third party, including Moneyshelf. The savings banks maintained that they would not only refuse any liability in case of fraud, but that they would reserve the right to cancel the banking relationship with the client altogether should he or she access the account via Moneyshelf. Moreover the marketing campaign for Moneyshelf which depicted procreating animals was not very appealing to a largely conservative German retail banking segment.

Bundling as the central value propostion

Yet, Deutsche Bank got something right: the topic of bundling. As much as Fintech is about unbundling of banking services, a convenience loving customer does not want to sign up with Fintech Firm A to buy DJI stocks, with Fintech company B to convert some FX and with Fintech enterprise C to set up a financial plan. The levels of user experience and thus user expectations have never been higher than today. Hence, the emancipated banking client of nowadays would expect all of these services offered by one single provider and being accessible via one user interface (UI). Banking platforms such as N26, Moven, Bankin’ and Simple prove that the theme of bundling is highly topical as they oftentimes put together the services of a range of Fintech firms and offer them seamlessly through one UI.

The sophisticated future of bundling

However, the future of bundling will be much more sophisticated than that. Clients will expect not only expect cost-efficient but dynamic bundles. For instance, whereas payment provider A may be ideal for one money transfer from country X to country Y, it maybe payment provider B for the next transaction. Clients will not care which contractual obligations the platform is tied to, but the customer will expect the most cost-efficient Fintech firm to take over the task at hand. The same goes for stock brokerage or financial planning. The client will rightly demand to execute via the most cost-efficient broker and to set-up the financial plan with that one Fintech firm he or she sees most suitable. It will be the task of the platform owner or “bundle”, to tap into the Fintech eco-system to always find the most suitable service provider. The bundler must to put together these services for the consumer seamlessly and in a highly transparent fashion.

The race for bundling is on

The race for the best bundler will be open to Fintech firms and incumbent banks alike. This time, however, banks will no longer have a head-start for two reasons: first, a range of highly professional financial data aggregators such as eWise exist nowadays which can provide the necessary services off-the-shelf. Secondly an overhaul of EU legislation will update the rights and responsibilities of account information service providers, permitting intermediaries to obtain the account access information from clients. This change in legislation will come into effect in 2018 and it will be the starter’s gun for a European bundlers’ race in financial services.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

On March 10th, 2000, the burst of the so called Dot-Com Bubble started. After nearly doubling within only one year and peaking at 5048, the NASDAQ index fell as much as 78% in the aftermath of that day. Clearly, estimates vary, but it is said that the astonishing sum of USD 1.7 trillion were lost in less than a year.

Shedding the “e-“ prefix and “.com” suffix

The vanishing assets were the most obvious and immediate consequences of this remarkable period. Yet, the burst of the Dot-Com Bubble had also other ramifications. Expressions, names and language changed rather abruptly. While the “e-“ prefix was widely adopted for products and firms before March 10th, companies were now shedding the “-e” attribute faster than an Alaskan Malamute its winter coat during springtime. The same happened to the “.com” suffix. All of sudden no firm wanted to be associated with eCommerce any longer; bricks and mortar became fashionable again. Even email turned into mail and – to make it distinguishable – to what was previously termed mail, postal mail became snail mail.

Absorbing Dot-Com technology

Yet, the eCommerce and Dot-Com technology did not disappear. On the contrary, the innovations made in the years leading up to the bubble burst prevailed. Web technologies have never been as pervasively applied as today. A Web sales channel or at least an information outlet has become a standard for most enterprises in the western world. Hence, Internet technology did not disappear with the burst of the Dot-Com Bubble. Rather than that, it was absorbed, transformed and adopted by the majority of firms and turned into a business standard.

After the burst of the Fintech bubble

The same will happen to Fintech. It is safe to say that we will see a Fintech bubble burst in the years to come. Turning into an outcast in the eyes of investors Fintech will then disappear as a label. However, a good share of the innovations brought forward by Fintech firms will then be absorbed by other players, such as by incumbent banks, insurers and software companies.

In 1996 Wesley Willis released his album “Rock ‘n’ Roll Will Never Die”. The Rock ‘n’ Roll that evolved in the United States during the late 1940s and early 1950s has ever since been absorbed, transformed and adopted by other musicians around the world. In that sense Rock ‘n’ Roll is truly immortal. The same will apply to Fintech.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

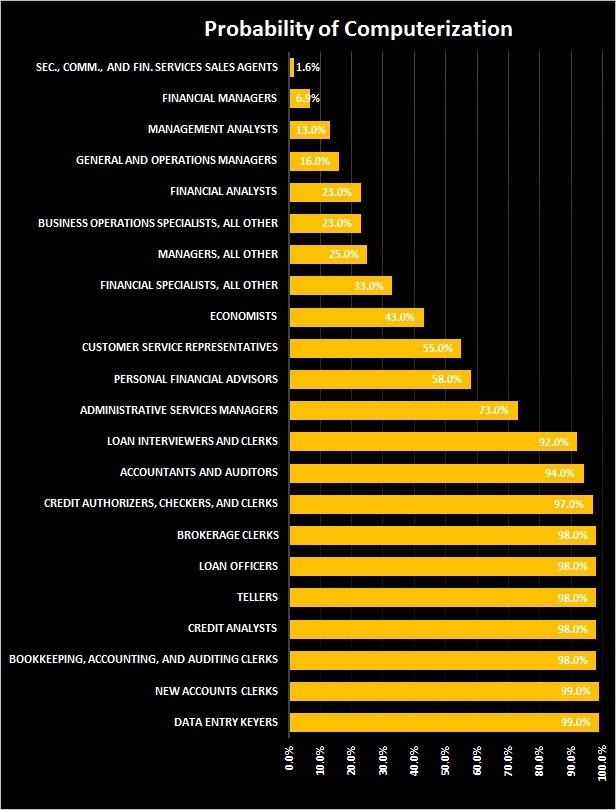

Sie sind, mit ihrer Mischung aus hochkompliziertem Denken, Intuition und mitunter leidenschaftlich verteidigten Grundsätzen, sozusagen die Theologen des Kapitalismus: die Ökonomen. Kaum ein Berufsstand im Bankbereich genießt so hohes intellektuelles Ansehen. Nirgendwo sonst spielt akademisches Denken im Geschäft eine vergleichbar große Rolle. Aber wie wahrscheinlich ist es, dass auch im Jahr 2033 Banken noch Ökonomen beschäftigen? Nach Meinung von Patrick Schüffel, Finanz-Professor im schweizerischen Freiburg, wird dieser Job zwischen 2023 und 2033 mit einer Wahrscheinlichkeit von 43 Prozent vom Computer übernommen. Ein Beispiel dafür, dass der digitale Kollege, der uns in den letzten Jahren mehr und Routinearbeit abgenommen hat, künftig auch intellektuelle Aufgaben übernimmt.

Schüffel stützt sich bei seiner Prognose auf eine Arbeit von Carl Benedikt Frey und Michael Osborne mit dem Titel “The Future of Employment”. Darin haben die beiden Wissenschaftler, gestützt auf offizielle Jobbeschreibungen der US-Regierung, 702 Berufe untersucht. Sie prüften mit einem mathematischen Modell, das auf Basis bisheriger Trends Prognosen erstellte, die Wahrscheinlichkeit des Verschwindens von Jobprofilen. Ihre Schlussfolgerungen sind dramatisch: “Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Das heißt, die entsprechenden Tätigkeiten können irgendwann in der Zukunft, vielleicht in zehn oder 20 Jahren, automatisiert werden.”

Schüffel hat gezielt die Daten für die Bankbranche für das Jahrzehnt bis 2033 aus der Studie herausgezogen. Die Ergebnisse zeigen eine große Bandbreite. So liegt die Wahrscheinlichkeit, dass Verkäufer im Wertpapierbereich überflüssig werden, bei nur 1,6 Prozent. Auf der anderen Seite sind “persönliche Finanzberater” mit 58 Prozent Risiko in hohem Maße bedroht. Noch schlimmer sieht es für Leute aus, die lediglich per Hand Daten erfassen: Mit 99 Prozent Risiko hat der Beruf kaum eine Überlebenschance. Dasselbe gilt aber mit 98 Prozent auch für Buchhalter und Kreditsachbearbeiter. Zum Teil enthält die Aufstellung allerdings kaum erklärbare Differenzen: Finanz-Analysten sind nur zu 23 Prozent bedroht, Kredit-Analysten dagegen zu 98 Prozent.

Das letzte Beispiel zeigt die Grenzen derartiger Prognosen. Letztlich handelt es sich um Gedankenspiele, bei denen der eigentliche Wert weniger in den Prozentzahlen liegt als darin, Denkanstöße zu geben. Ein wichtiger Punkt ist dabei: Arbeiten, die allein eine hohe abstrakte Intelligenz erfordern, gelten als durchaus ersetzbar. Je mehr hingegen soziale Intelligenz und Kreativität gefragt sind, desto weniger Chancen hat Kollege Computer. Daher sind Verkäufer schwer zu ersetzen, auch wenn sie vielleicht weniger abstrakte Intelligenz brauchen als Ökonomen.

Soziale Kompetenz als ein Ausweg Ausschlaggebend für die Einschätzung der jeweiligen Berufe ist daher, wie die damit verbundenden Aufgaben eingeschätzt und gewichtet werden. Besteht die Aufgabe des Ökonomen vor allem darin, eine Konjunkturprognose für das nächste Quartal abzugeben? Dann hat der Kollege Computer eine gute Chance, ihn abzulösen. Schon heute gibt es Unternehmen wie etwa Now-Cast, bei denen selbstlernende Software kurzfristige Prognosen übernimmt. Oder besteht die Aufgabe der Ökonomen eher darin, Daten zu erklären und Rahmenbedingungen für die wirtschaftliche Entwicklung zu analysieren? Da tut sich der Computer schon schwerer. Viele Bank-Ökonomen arbeiten zudem de facto in der Kundenbetreuung. Sie unterhalten sich mit Großkunden über ökonomische Fragen.

Das dient nicht nur dazu, harte Schlussfolgerungen, etwa für Investitionen, logisch abzuleiten. Anleger, die ihre Entscheidungen unter hoher Unsicherheit treffen müssen, suchen versierte Gesprächspartner, mit denen sie die Last dieser Unsicherheit teilen können. Bei dieser Aufgabe ist das persönliche Gespräch durch nichts zu ersetzen, nicht einmal durch Videokonferenzen, geschweige denn den Computer.

Das Beispiel zeigt, dass der Computer viele Berufe nicht ersetzt, sondern sie verändert und die Gewichte verschiebt. So gibt es etwa bei freien Finanzberatern in den USA den Trend, Anlage-Entscheidungen tatsächlich Computern, den sogenannten Robo-Advisern, zu überlassen. Kernaufgabe des Beraters ist dann nicht mehr, dem Kunden einen angeblich heißen Aktientipp zu geben. Vielmehr muss der Dienstleister helfen, eine Einschätzung seiner finanziellen Situation und Risikobereitschaft herzuleiten. Diese kann dann Grundlage für die maschinelle Verwaltung eines Depots werden.

Heute schon gibt es auch Firmen, die vom Handel an den Kapitalmärkten leben, ohne einen einzigen Händler zu beschäftigen. Die Aufträge werden vom Computer erledigt. Aber die jeweilige Software entsteht in Zusammenarbeit von Computer- und Kapitalmarktexperten. Für viele Banker dürfte gelten, was Frey und Osborne als Schlussfolgerung ziehen: “Damit Beschäftigte das Rennen gewinnen, müssen sie kreative und soziale Kompetenz erwerben.”

ZITATE FAKTEN MEINUNGEN

Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Carl Benedikt Frey, Michael Osborne Professoren in Oxford

Fintech is steaming ahead at an incredible pace. What robots used to be for the automotive industry, algorithms have become to the banking industry.

Common wisdom had it that one’s job would be secure if one was well educated and kept up-to-date on the job. Now, however, we are increasingly facing a situation when even highly sophisticated occupations such as personal finance advisors as well as accountants and auditors will fall prey to digitalization.

The Future of Employment

In their 2013 study “The Future of Employment” Karl Benedikt Frey and Michael Osborne estimated the probability of computerization for 702 professions based on three factors: perception and manipulation tasks, creative intelligence tasks and social intelligence tasks.

Applied to Banking

Of those occupations examined by Frey and Osborne I have extracted those that I find relevant to the banking industry. The percentage figure displayed indicates the likelihood of that profession being computerized in “a decade or two”, i.e. between 2023 and 2033.

Occupation: Probability of Computerization

Sec., Commod., and Fin. Services Sales Agents: 1.6%

Financial Managers: 6.9%

Management Analysts: 13.0%

General and Operations Managers: 16.0%

Financial Analysts: 23.0%

Business Operations Specialists, All Other: 23.0%

Managers, All Other: 25.0%

Financial Specialists, All Other: 33.0%

Economists: 43.0%

Customer Service Representatives: 55.0%

Personal Financial Advisors: 58.0%

Administrative Services Managers: 73.0%

Loan Interviewers and Clerks: 92.0%

Accountants and Auditors: 94.0%

Credit Authorizers, Checkers, and Clerks: 97.0%

Tellers: 98.0%

Loan Officers: 98.0%

Credit Analysts: 98.0%

Brokerage Clerks: 98.0%

Bookkeeping, Accounting, and Auditing Clerks: 98.0%

New Accounts Clerks: 99.0%

Data Entry Keyers: 99.0%

Dr. Patrick Schüffel, A.Dip.C., M.I.B., Dipl.-Kfm.

Professsor

Institute of Finance

Haute école de gestion Fribourg

Chemin du Musée 4

CH-1700 Fribourg

patrick.schueffel@hefr.ch, www.heg-fr.ch

Currently the Annual Academy of Management (AoM) Meeting is taking place in Anaheim, California. Some 10’000 Management scholars from 88 countries are meeting to discuss the current affairs of Management and its outlooks. In more than 2’500 sessions topics are discussed from the disciplines of Entrepreneurship, Technology and Innovation Management, Organization Development and Change, and Operations Management, just to name a few. The meeting program spans a whopping 608 pages and contains literally hundreds of thousands of words. Yet one word is missing: FINTECH!

Already today more than three dozen Fintech unicorns exist, most of which are not even five years of age. Moreover we are witnessing the appearance of novel Fintech companies almost on a daily basis. This development has caught the attention of business people, regulators and politicians alike. Yet, this development has largely gone unnoticed by the academic world as far as management sciences are concerned. Clearly, there are noteworthy exceptions from this rule, but at large Fintech is simply not existing in this academic setting.

This situation gives rise to several questions. For instance, how do we educate Management students for today’s banking and finance world if the Fintech phenomenon remains untouched? How do we train executives?How does academia intend to give sound advice to policy makers in view of this neglect? If the ultimate purpose of science – among others – is to explain, control and predict, academia must swing into action and intensify its efforts in the field of Fintech.

I therefore also strongly welcome efforts such as the ones by Thomas Puschmann of the University of Zurich who is actively building a bridge between the practical Fintech world and academia by establishing the “Swiss Fintech Innovations” association as a port of call for practice and academia alike.

In Luxembourg Anne-Laure Mention is one of the commendable academics at CRP Henri Tudor who attempts to narrow the gulf between innovation in financial services in practice and academia.

If there are other such initiatives in other countries, please do drop me line! I am keen to learn!

Dr. Patrick Schüffel, A.Dip.C., M.I.B., Dipl.-Kfm. Professsor

Haute école de gestion Fribourg

Institute of Finance

Chemin du Musée 4

CH-1700 Fribourg patrick.schueffel@hefr.ch, www.heg-fr.ch

If you want to read the complete edition of Best of the Web, Fiancial edition 13. Sep 2016, click

If you want to read the complete edition of Best of the Web, Fiancial edition 13. Sep 2016, click

Currently the Annual

Currently the Annual