Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Kunden erwarten zunehmend maßgeschneiderte, individuelle Angebote. Produktindividualisierung und Mass-Customization liegen im Trend. Auch die Zukunft von Banken und Sparkassen hängt angesichts der Konkurrenz durch FinTechs davon ab.v

Moderne Fertigungstechnologien erlauben, was vor wenigen Jahrzehnten noch unvorstellbar war. Wenn wir wollen, können wir heute Produkte aus der Massenproduktion beziehen, die dennoch auf unsere individuellen Bedürfnisse zugeschnitten sind. Michael Dell machte lediglich den Anfang, als er damit anfing, in großem Maßstab PCs nach individuellen Anforderungen zusammenzubauen. Heute bestellen wir unsere maßgeschneiderten Turnschuhe bei Nike ID, tragen ein einzigartiges T-Shirt von Spreadshirt und essen M & M’s mit unserer eigenen Initialen. Der Trend zur Mass-Customization endet jedoch nicht im verarbeitenden Gewerbe. Im Gegenteil, bereits heute können wir die Auswirkungen der Mass Customization in der Finanzdienstleistungsbranche beobachten, beispielsweise dort, wo Robo-Advisor die Kundenportfolios der Retail-Kundschaft anpassen. Aber das ist nicht der Endpunkt der Evolution. Es ist nur der Anfang, der schlussendlich zu maßgeschneiderten Banken führen wird.

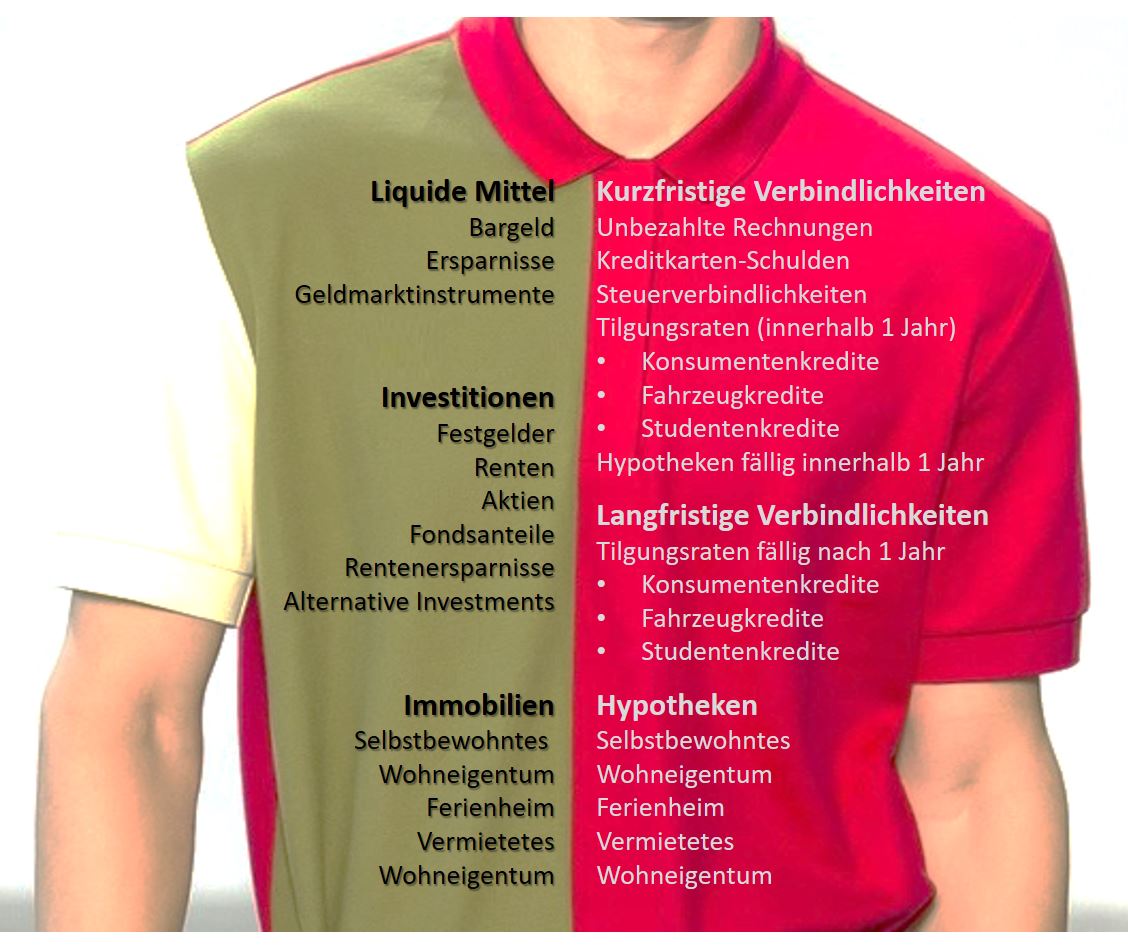

Die individuelle Bilanz eines Bankkunden

Ob man es mag oder nicht, jeder einzelne von uns besitzt seine eigene ganz persönliche Bilanz: Auf der Aktivseite besitzen wir flüssige Vermögenswerte wie das Bargeld, das wir in unseren Geldbeuteln herum tragen, das Geld auf unseren Giro- und Sparkonten sowie Geldmarktinstrumente. Unsere persönlichen Anlagen umfassen möglicherweise mittelfristige Schuldverschreibungen, Anleihen, Aktien, Investmentfonds, Rentenersparnisse und / oder alternative Anlagen. Schließlich können wir auch sehr illiquide Werte besitzen wie eigengenutzte Immobilien sowie Ferienhäuser oder sogar vermietetes Wohneigentum.

Persönliche Bilanz

Auf der Passivseite verfügen wir ebenfalls über eine Vielzahl von Positionen. Die kurzfristigen Verbindlichkeiten können unbezahlte Rechnungen, Kreditkartenguthaben, fällige Steuern, kurzfristig fällige Raten- und Konsumentenkredite, Kfz-Darlehen, Studentenkredite, Hypotheken mit kurzen Restlaufzeiten usw. beinhalten. Langfristige Verbindlichkeiten können jegliche Verbraucher-, Auto- oder Studentenkredite umfassen, die nach einem Jahr fällig sind. Zu guter Letzt, können wir auch Hypotheken für unser primäres Wohneigentum Residenz und / oder Ferienwohnungen und / oder Mietobjekt aufgenommen haben.

So individuell wie wir als Menschen sind, so individuell sind auch unsere persönlichen Bilanzen. Doch was wir als Verbraucher gemeinsam haben, ist, dass wir freiwillig oder unfreiwillig diese Bilanzen bewirtschaften. Wir führen Treasury-Funktionen auf unseren persönlichen Bilanzen durch, indem wir Rechnungen und Raten bezahlen, Geld von einem Konto zum anderen übertragen, indem wir Investition in Aktien tätigen oder durch die Rückgabe von Investmentfondsanteilen etc.

Die FinTech Alternative

In der westlichen Welt unterhalten viele Verbraucher Beziehungen zu einer oder zwei Banken – oftmals Universalbanken -, die allen Bedürfnissen entsprechen, welche sich aus den besagten Treasury-Transaktionen ergeben. Dennoch erhält das Serviceangebote der Universalbanken zunehmend Konkurrenz von FinTech-Firmen, deren Anzahl und Vielfalt der FinTech-Angebote kontinuierlich steigt. Sie bieten typischerweise eine sehr schmale Bandbreite von Services an, sind dabei jedoch hochspezialisiert und meist mit einer besseren User-Experience und günstigeren Preisen verbunden.

Wenn ein Bankkunde beispielsweise kleinere Summen sparen möchte, bieten FinTech-Firmen wie Creditgate24, LendingClub oder Crowdcube Angebote zur Optimierung von liquiden Mitteln. Um langfristige Investitionen zu verwalten, kann man sich an Anbieter wie Wealthfront, Moneyfarm, Nutmeg, Addepar etc. wenden. Auch auf der Passivseite gibt es eine breite Palette von FinTech-Firmen, die sich den verschiedenen Passivposten widmen. So können die kurz- und mittelfristigen Verbindlichkeiten beispielsweise durch die Verwendung von Affirm, Borro, Lendable, Prosper etc. optimiert werden.

Um Geld von einem Akteur bzw. Konto zu einem anderen zu übertragen, kann der Verbraucher unter Dutzenden von Zahlungsdienstleistern wie TransferWise, LiquidPay, Paypal und dergleichen wählen. Für den Wertpapierhandel kann sich der Kunde sich an eToro oder Robinhood wenden. Sogar das Spenden von Geld wird mit FinTech-Anbietern wie Elefunds komfortabler und effizienter.

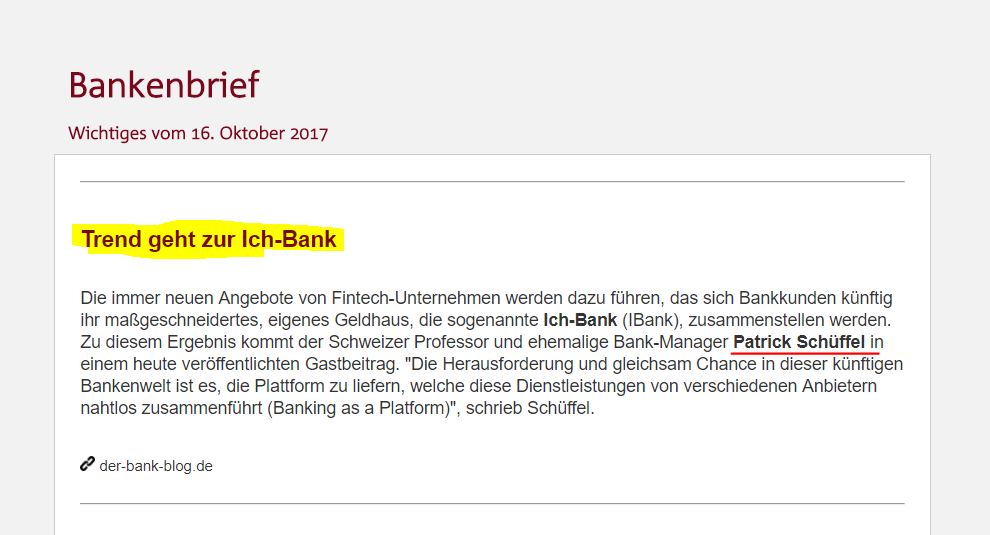

Diese neuen Arten von Finanzdienstleistern, die ihre Nischen auf den einzelnen Gliedern der Wertschöpfungskette von Universalbanken gefunden haben, versprechen in der Regel nicht nur ihren Kunden eine bessere Nutzererfahrung, sondern auch geringere Kosten. Was für die nahe Zukunft vorhersehbar ist, ist, dass die Kunden es nicht länger akzeptieren werden, durch den Lock-in Effekt mit ein oder zwei Banken dauerhaft verbunden zu sein, sondern dass sie eine ganze Palette von verschiedenen Finanzdienstleistern nutzen werden. Schließlich wird diese Entwicklung dazu führen, dass jeder Kunde seine eigene Bank, die IBank , wie ich sie nenne, zusammenstellen wird. IBank ist dabei im Sinne von „Ich Bank“ gemeint und nicht zu verwechseln mit den iBank-Angeboten von Barclays, der Bank von Georgia, Fransabank, BCU etc.

Der Zusammenbau der IBank

Die IBank umfasst eine Auswahl von Dienstleistungen, welche von bestimmten FinTech-Unternehmen angeboten werden, und die von den einzelnen Kunden handverlesen werden. Dies kann dynamisch und ad-hoc oder auf einer dauerhafteren Basis geschehen. Der Kunde – oder ein übergreifender Algorithmus, der für diesen Zweck erarbeitet wurde – könnte so zum Beispiel von Fall zu Fall entscheiden, welcher Zahlungsdienst für eine individuelle Überweisung der bestgeeignetste wäre. Ebenso könnte der Kunde oder das System entscheiden, welcher Hypothekenanbieter idealerweise gewählt werden soll, um eine Hypothek abzulösen.

Es ist wichtig zu verstehen, dass Kunden künftig von „Banken“ Gebrauch machen werden, die ebenso persönlich auf die Bedürfnisse des Kunden zugeschnitten sein werden, wie es die individuelle Bilanz der Verbrauchers erfordert. Die Herausforderung und gleichsam Chance in dieser künftigen Bankenwelt ist es, die Plattform zu liefern, welche diese Dienstleistungen von verschiedenen Anbietern nahtlos zusammenführt (Banking as a Platform). Diejenigen Anbieter, die es schaffen, eine übergreifende Struktur zusammenzustellen und zu pflegen, welche es vermag, die Vielfalt der Dienstleistungsangebote von FinTech-Anbietern reibungslos zu integrieren, werden eine vielversprechende Zukunft haben. Angesichts einer Finanzdienstleistungsbranche, die zunehmend atomisiert wird, ist dies sicherlich ein lohnenswerter Ausblick.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

The full article can be accessed here. (French only)

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Avec son numéro d’avril 2017, le journal suisse «Bilan» a récemment publié un supplément sur Fintech en Suisse. J’étais ravi de constater que l’éditeur a cité ma définition de Fintech, précédemment publiée dans le Journal of Innovation Management. Comme la publication originale était en anglais, la traduction française publiée par Bilan est la suivante:

«Fintech est une nouvelle industrie financière qui déploie la technologie pour améliorer les activités financières.»

(Patrick Schueffel tel que cité par Comment la suisse se profile comme un centre Fintech compétitif, Bilan 4/2017, supplément Fintech – Construire la finance de demain, p.6)

“Fintech is a new financial industry that applies technology to improve financial activities”(Schueffel, 2016; p. 45)

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

“Fintech is a new financial industry that applies technology to improve financial activities.” (Schueffel, 2016; p. 45)

This is the definition I derived after examining more than 200 scholarly articles that were published over a period of 40 years and which are referencing the word Fintech in one way or the other. Building on the commonalities of the definitions that found entry into those peer-reviewed journals I distilled the definition provided above.

I am proud that my work withstood the rigorous double-blind peer review process of the Journal of Innovation Management and was published these days.

As the Journal of Innovation Management is an open access journal you can retrieve the full text by using the following link:

Schueffel, P. (2016). Taming the Beast: A Scientific Definition of Fintech. Journal of Innovation Management, 4(4), 32-54.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.

Have you even tried to explain the Blockchain concept to a seasoned private banker? Have you tried to describe the notion of a distributed ledger to this type of auditorium? And have you experienced the same result as I have over and over again: have you, too, just banged your head against a brick wall? I pondered the question why it was so much harder to explicate the concept to alleged banking experts than to first-year business students.

Use the right vocabulary

After numerous futile explanation attempts, it dawned on me. I was using the wrong vocabulary. Using the word ledger is counterproductive to the cause. When talking about a ledger, the traditional banker immediately translates that term into “bankbook” and that is the book in which the bank keeps all records of all customers adding and taking money from their bank accounts. It is thus the holy grail of private banking. Distributing the holy grail is inconceivable to many a private banker.

At that point it then hardly matters if you continue to explain that the users of the Blockchain are typically anonymized. It is almost futile to further explicate that, for instance, Bitcoin accounts are not tied to the identity of users and that anyone can create new and completely random Bitcoin accounts at any time, without the need to submit any personal information to any party. You have lost them already. Hence, what I found helpful in this situation is to refrain from using the term “ledger” altogether. Instead I call it distributed data base or distributed accounting system.

Give them a hands-on example

A friend of mine and design thinking pioneer, Michael Lewrick recently recommended me to do a hands-on exercise in particularly tough cases. Individually assign a random yet different number to every one of the ten bankers that are sitting in a room with you and have each of them note down their number and favourite colour on a separate sheet of paper. Have them pass on the paper to another participant and everyone repeats the exercise. Do so altogether ten times. In the end, everyone holds a list of 10 numbers and favourite colours in their hands. At this stage you can ask a) “What is Bob’s favourite colour?” – the others shouldn’t be able to tell as Bob’s identity has been anonymized. Yet you can also ask Bob, whether the correct colour is listed on his sheet – which should clearly be the case. And b) you can ask someone to now commit a “fraud”, i.e. to change the favourite colour of one participant – which should be nearly impossible unless the tasked fraudster does so on ten sheets of paper with the nine remaining group members agreeing. This exercise nicely explains some of the key features of the Blockchain and monies based thereon.

It’s worth trying

These two measures combined, using audience specific language and a hands-on exercise should therefore do the job. It certainly deserves a try. The Blockchain concept is too important as we could afford leaving private bankers behind. Happy explaining!

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

The number and diversity of Fintech offerings is soaring. As banking clients increasingly often enjoy not only a better user experience, but also cheaper rates at Fintech firms, their willingness to be locked-in with one or two universal banks diminishes. Henceforth clients will gradually assemble their own individual “banks”, comprising a range of offerings from different Fintech companies. Those firms which will be able to provide an overarching structure to seamlessly wrap the multitude of Fintech offerings will experience their heydays.

Modern production technology allows what would have been inconceivable only a few decades ago. If we want, we can have products of mass production tailored to our needs nowadays. Dell made only the beginning when first assembling PCs to our requests on a large scale. Today we order our tailored sneakers at Nike ID, wear a unique t-shirt from Spreadshirt and eat M&M’s sporting our very own initials. Yet, the trend of mass customization did not stop in the manufacturing sector. We can already observe its ramifications in the financial services industry where Robo-Advisors offer retail customers to tailor their client portfolios. But this is not the end point of the evolution. It is the mere beginning which will eventually lead to tailored banks.

The personal balance sheet

Like it or not, every single one of us carries his or her own very personal balance sheet: On the asset side, we have liquid asset positions such as the cash that we have in our wallets, the money on our current accounts, our savings accounts or money market instruments. Our personal investments may comprise medium term notes, bonds, stocks, mutual funds, pension savings and/or alternative Investments. Finally, we may possess highly illiquid real estate investments such as our primary residences, vacation homes or even property that we rent out.

On the liability side we may also have a variety of items. Current liabilities may include unpaid bills, credit card balances, taxes due, installment loans due in the short run, consumer loans, car loans, student loans, mortgages due within one year etc. Non-current liabilities may include any consumer, car or student loan that is due after one year. Last but not least, we may have mortgage debt for our primary residence and/or vacation homes and/or rental property.

Hence, as individual as we are as human beings, as individual are our personal balance sheets. Yet, what we do have in common is that we willingly or unwillingly manage these balance sheets. We carry out treasury functions on our personal balance sheets by paying bills and installments, transferring money from one account to another, by investing in shares or by redeeming mutual funds etc.

The Fintech Alternative

So far many consumers in the western world have ties to one or two banks, oftentimes universal banks, that cater to all of the needs resulting from these treasury transactions. Yet, the service offerings of universal banks are increasingly rivaled by Fintech firms that offer a narrow, yet highly specialized service or product.

If you have a little cash to spare, Fintech firms such as Creditgate24, LendingClub or Crowdcube, have offerings for optimizing liquid assets. To manage longer term investments one can turn to providers such Wealthfront, Moneyfarm, Nutmeg, Addepar etc. On the liability side, too, there is a vast array of Fintech companies jockeying for position. Current and medium term liabilities may be optimized by using Affirm, Borro, Lendable, Prosper etc.

In order to transfer money from one provider or account to another the consumer can chose among dozens of payment providers such as TransferWise, LiquidPay, Paypal and the likes. For trading purposes the client may want to turn to eToro or Robinhood. Even donating money becomes easier and less burdensome with Fintech providers such as Elefunds.

These new type of financial services providers that found their niches on specific links of the value chains of universal banks typically not only promise their clients a better user experience, but also lower costs. What is thus foreseeable for the near future is that clients will no longer accept to be locked-in with one or two banks, but that they will make use of a range of financial service providers. Eventually every user will assemble his or her very own bank, the IBank* as I call it.

Assembling the IBank

The IBank will comprise a selection of services provided by specific Fintech companies handpicked by the individual client. This can happen dynamically and on an ad-hoc basis or on a more permanent base. The client – or an overlaying algorithm for that matter – may decide on a case-by-case basis which payment service would be optimal for a specific transfer. On a more longer term basis one mortgage provider may be chosen until the renewal of the mortgage is due.

What is important to note, however, is that clients will make use of tailored “banks” which may be as personal as their individual balance sheet. The challenge and opportunity in this future banking world will be to provide the glue that seamlessly keeps together these services provided by different providers. Those providers who manage to assemble and maintain an overarching structure that smoothly integrates the multitude of service offering of Fintech providers will have a bright future in finance services world which is being ever more atomized.

*IBank like “I bank” – not to be mistaken with the iBank offerings by Barclays, The Bank of Georgia, Fransabank, BCU and so on.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Link zum Bankbrief:

Link zum Bankbrief:

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.