![]()

Nr. 168 vom 31.08.2016 Seite 030

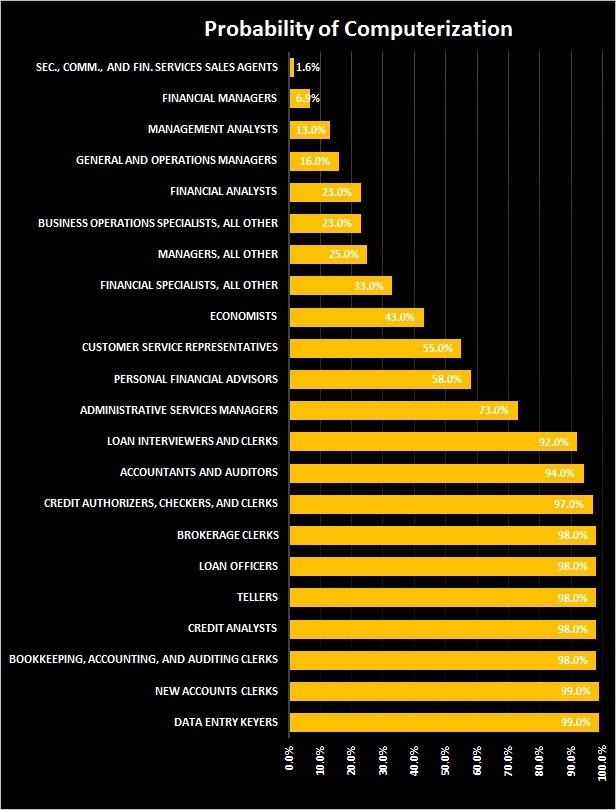

Sie sind, mit ihrer Mischung aus hochkompliziertem Denken, Intuition und mitunter leidenschaftlich verteidigten Grundsätzen, sozusagen die Theologen des Kapitalismus: die Ökonomen. Kaum ein Berufsstand im Bankbereich genießt so hohes intellektuelles Ansehen. Nirgendwo sonst spielt akademisches Denken im Geschäft eine vergleichbar große Rolle. Aber wie wahrscheinlich ist es, dass auch im Jahr 2033 Banken noch Ökonomen beschäftigen? Nach Meinung von Patrick Schüffel, Finanz-Professor im schweizerischen Freiburg, wird dieser Job zwischen 2023 und 2033 mit einer Wahrscheinlichkeit von 43 Prozent vom Computer übernommen. Ein Beispiel dafür, dass der digitale Kollege, der uns in den letzten Jahren mehr und Routinearbeit abgenommen hat, künftig auch intellektuelle Aufgaben übernimmt.

Schüffel stützt sich bei seiner Prognose auf eine Arbeit von Carl Benedikt Frey und Michael Osborne mit dem Titel “The Future of Employment”. Darin haben die beiden Wissenschaftler, gestützt auf offizielle Jobbeschreibungen der US-Regierung, 702 Berufe untersucht. Sie prüften mit einem mathematischen Modell, das auf Basis bisheriger Trends Prognosen erstellte, die Wahrscheinlichkeit des Verschwindens von Jobprofilen. Ihre Schlussfolgerungen sind dramatisch: “Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Das heißt, die entsprechenden Tätigkeiten können irgendwann in der Zukunft, vielleicht in zehn oder 20 Jahren, automatisiert werden.”

Schüffel hat gezielt die Daten für die Bankbranche für das Jahrzehnt bis 2033 aus der Studie herausgezogen. Die Ergebnisse zeigen eine große Bandbreite. So liegt die Wahrscheinlichkeit, dass Verkäufer im Wertpapierbereich überflüssig werden, bei nur 1,6 Prozent. Auf der anderen Seite sind “persönliche Finanzberater” mit 58 Prozent Risiko in hohem Maße bedroht. Noch schlimmer sieht es für Leute aus, die lediglich per Hand Daten erfassen: Mit 99 Prozent Risiko hat der Beruf kaum eine Überlebenschance. Dasselbe gilt aber mit 98 Prozent auch für Buchhalter und Kreditsachbearbeiter. Zum Teil enthält die Aufstellung allerdings kaum erklärbare Differenzen: Finanz-Analysten sind nur zu 23 Prozent bedroht, Kredit-Analysten dagegen zu 98 Prozent.

Das letzte Beispiel zeigt die Grenzen derartiger Prognosen. Letztlich handelt es sich um Gedankenspiele, bei denen der eigentliche Wert weniger in den Prozentzahlen liegt als darin, Denkanstöße zu geben. Ein wichtiger Punkt ist dabei: Arbeiten, die allein eine hohe abstrakte Intelligenz erfordern, gelten als durchaus ersetzbar. Je mehr hingegen soziale Intelligenz und Kreativität gefragt sind, desto weniger Chancen hat Kollege Computer. Daher sind Verkäufer schwer zu ersetzen, auch wenn sie vielleicht weniger abstrakte Intelligenz brauchen als Ökonomen.

Soziale Kompetenz als ein Ausweg Ausschlaggebend für die Einschätzung der jeweiligen Berufe ist daher, wie die damit verbundenden Aufgaben eingeschätzt und gewichtet werden. Besteht die Aufgabe des Ökonomen vor allem darin, eine Konjunkturprognose für das nächste Quartal abzugeben? Dann hat der Kollege Computer eine gute Chance, ihn abzulösen. Schon heute gibt es Unternehmen wie etwa Now-Cast, bei denen selbstlernende Software kurzfristige Prognosen übernimmt. Oder besteht die Aufgabe der Ökonomen eher darin, Daten zu erklären und Rahmenbedingungen für die wirtschaftliche Entwicklung zu analysieren? Da tut sich der Computer schon schwerer. Viele Bank-Ökonomen arbeiten zudem de facto in der Kundenbetreuung. Sie unterhalten sich mit Großkunden über ökonomische Fragen.

Das dient nicht nur dazu, harte Schlussfolgerungen, etwa für Investitionen, logisch abzuleiten. Anleger, die ihre Entscheidungen unter hoher Unsicherheit treffen müssen, suchen versierte Gesprächspartner, mit denen sie die Last dieser Unsicherheit teilen können. Bei dieser Aufgabe ist das persönliche Gespräch durch nichts zu ersetzen, nicht einmal durch Videokonferenzen, geschweige denn den Computer.

Das Beispiel zeigt, dass der Computer viele Berufe nicht ersetzt, sondern sie verändert und die Gewichte verschiebt. So gibt es etwa bei freien Finanzberatern in den USA den Trend, Anlage-Entscheidungen tatsächlich Computern, den sogenannten Robo-Advisern, zu überlassen. Kernaufgabe des Beraters ist dann nicht mehr, dem Kunden einen angeblich heißen Aktientipp zu geben. Vielmehr muss der Dienstleister helfen, eine Einschätzung seiner finanziellen Situation und Risikobereitschaft herzuleiten. Diese kann dann Grundlage für die maschinelle Verwaltung eines Depots werden.

Heute schon gibt es auch Firmen, die vom Handel an den Kapitalmärkten leben, ohne einen einzigen Händler zu beschäftigen. Die Aufträge werden vom Computer erledigt. Aber die jeweilige Software entsteht in Zusammenarbeit von Computer- und Kapitalmarktexperten. Für viele Banker dürfte gelten, was Frey und Osborne als Schlussfolgerung ziehen: “Damit Beschäftigte das Rennen gewinnen, müssen sie kreative und soziale Kompetenz erwerben.”

ZITATE FAKTEN MEINUNGEN

Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Carl Benedikt Frey, Michael Osborne Professoren in Oxford

https://www.financial-career-bw.de/news-events/news/detailansicht/artikel/welche-bankjobs-der-computer-uumlbernimmt/

Currently the Annual

Currently the Annual