Jobangst, Digitalisierung, politische Umwälzungen: Das abgelaufene Jahr war heftig. Die Erschöpfung ist gross – auch bei Topmanagern. Was ihnen zu schaffen macht und wo sie Hilfe finden.

Ein Auszug aus dem Text:

Ein Auszug aus dem Text:

Bundling will be the next big Fintech topic after unbundling and platformization. Just as consumers got used to buying different food items at one single supermarket long time ago, they will expect one-stop-shops for financial services. Those “bundlers” that manage to seamlessly offer cost-efficient and dynamic bundles are well poised for success in this next race in the Fintech arena. Some important lessons can be learned from previous bundling attempts, such as Deutsche Bank’s “Moneyshelf”.

In 2002 Deutsche Bank started an immensely ambitious e-commerce project. The objective of the project by the name of „Moneyshelf“ was to establish a financial super market. The goal was to create a one stop shop for virtually any financial product a retail client could wish for – across any provider existing. The underlying idea was to provide off the shelf financial products from any makers and brands. The reasoning behind it was that consumers would also frequent supermarkets to conveniently buy various products across brands and manufacturers. A modern consumer would visit a single supermarket to purchase bread, sausages, apples, beverages, canned food and cleaning liquid. He or she would no longer go through the ordeal of visiting a bakery to buy bread, a butcher to shop for sausages, a local market to get some apples and then drop by yet another store to buy beverages and food before visiting the local drug store to buy cleaning liquid.

Creating a financial supermarket

In order to use such a financial supermarket the client was requested to deposit his access information to any other banking service with the Moneyshelf platform. Moneyshelf would then let the client consolidate and manage all of his or her accounts in one highly user-friendly frontend. In the background online banking interfaces programmed by Deutsche Bank developers would ensure the interoperability. Moneyshelf promised a quantum leap in transparency and price efficiency. A client who would have a securities account with bank A and be invested in mutual funds from fund provider B could then not only shop for a more cost-efficient securities account, but also a better performing and less costly mutual fund und would only be a mouse click away. All of this was paired with features such as personal financial planners which offered insights on the clients’ spending and financial behavior and a rich offering of financial information and possibilities of analysis.

Deutsche Bank ahead of times

Moneyshelf as it was envisioned by Deutsche Bank was offering the client a tremendously versatile platform to choose among a vast range of providers and products such as current and savings accounts, mutual funds, brokerage services, mortgages, even life insurances. Deutsche Bank sensed that clients would become more tech savvy and consider the threat to be very real that Deutsche Bank may soon be disintermediated as far as their retail segment was concerned. With the emergence of online brokers and their strong growth Deutsche Bank feared of getting skinned and decided to take the bull by the horns. Hence, should a client decide to do business with a different bank, then Deutsche Bank would make sure that it would at least get a share of those revenue streams bypassing them.

The bone of contention: depositing client data

In the end this business model failed big time. The other banks, especially the rather dominant German savings banks warned their clients that it would be a violation of their contractual obligations to deposit account access information with any third party, including Moneyshelf. The savings banks maintained that they would not only refuse any liability in case of fraud, but that they would reserve the right to cancel the banking relationship with the client altogether should he or she access the account via Moneyshelf. Moreover the marketing campaign for Moneyshelf which depicted procreating animals was not very appealing to a largely conservative German retail banking segment.

Bundling as the central value propostion

Yet, Deutsche Bank got something right: the topic of bundling. As much as Fintech is about unbundling of banking services, a convenience loving customer does not want to sign up with Fintech Firm A to buy DJI stocks, with Fintech company B to convert some FX and with Fintech enterprise C to set up a financial plan. The levels of user experience and thus user expectations have never been higher than today. Hence, the emancipated banking client of nowadays would expect all of these services offered by one single provider and being accessible via one user interface (UI). Banking platforms such as N26, Moven, Bankin’ and Simple prove that the theme of bundling is highly topical as they oftentimes put together the services of a range of Fintech firms and offer them seamlessly through one UI.

The sophisticated future of bundling

However, the future of bundling will be much more sophisticated than that. Clients will expect not only expect cost-efficient but dynamic bundles. For instance, whereas payment provider A may be ideal for one money transfer from country X to country Y, it maybe payment provider B for the next transaction. Clients will not care which contractual obligations the platform is tied to, but the customer will expect the most cost-efficient Fintech firm to take over the task at hand. The same goes for stock brokerage or financial planning. The client will rightly demand to execute via the most cost-efficient broker and to set-up the financial plan with that one Fintech firm he or she sees most suitable. It will be the task of the platform owner or “bundle”, to tap into the Fintech eco-system to always find the most suitable service provider. The bundler must to put together these services for the consumer seamlessly and in a highly transparent fashion.

The race for bundling is on

The race for the best bundler will be open to Fintech firms and incumbent banks alike. This time, however, banks will no longer have a head-start for two reasons: first, a range of highly professional financial data aggregators such as eWise exist nowadays which can provide the necessary services off-the-shelf. Secondly an overhaul of EU legislation will update the rights and responsibilities of account information service providers, permitting intermediaries to obtain the account access information from clients. This change in legislation will come into effect in 2018 and it will be the starter’s gun for a European bundlers’ race in financial services.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Moneyshelf ad

If you want to read the complete edition of Best of the Web, Fiancial edition 13. Sep 2016, click here.

If you want to read the complete edition of Best of the Web, Fiancial edition 13. Sep 2016, click here.

The full article can be accessed here. (German only)

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

![]()

Nr. 168 vom 31.08.2016 Seite 030

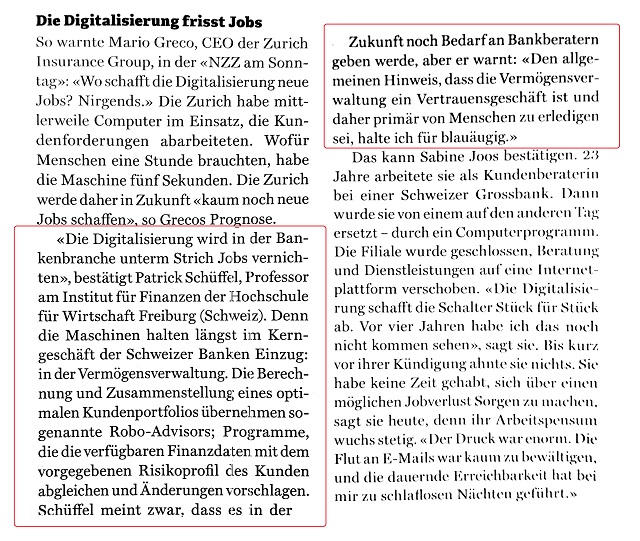

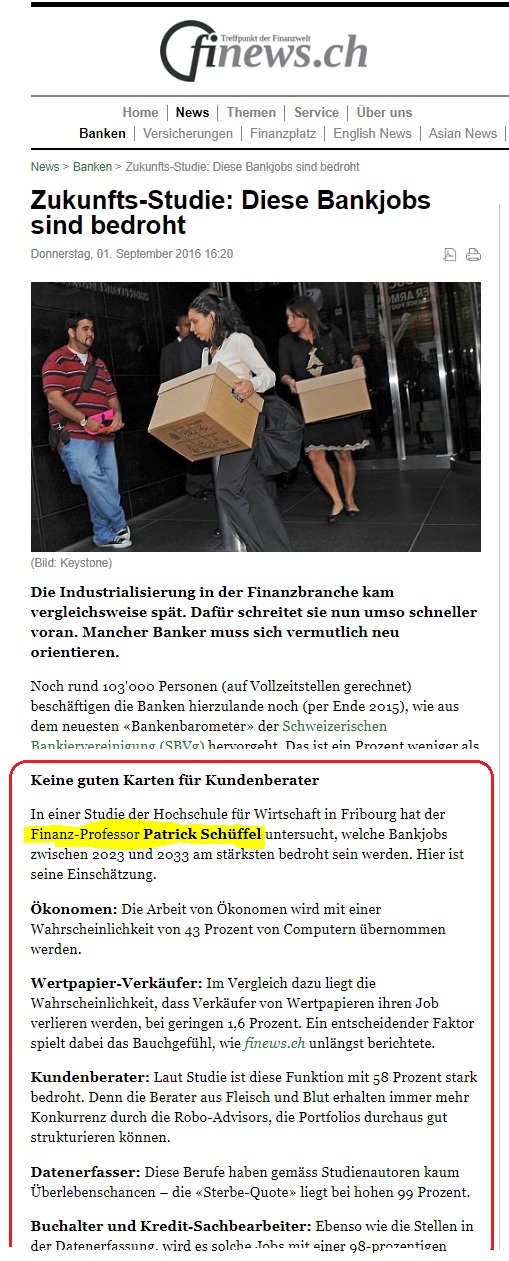

Sie sind, mit ihrer Mischung aus hochkompliziertem Denken, Intuition und mitunter leidenschaftlich verteidigten Grundsätzen, sozusagen die Theologen des Kapitalismus: die Ökonomen. Kaum ein Berufsstand im Bankbereich genießt so hohes intellektuelles Ansehen. Nirgendwo sonst spielt akademisches Denken im Geschäft eine vergleichbar große Rolle. Aber wie wahrscheinlich ist es, dass auch im Jahr 2033 Banken noch Ökonomen beschäftigen? Nach Meinung von Patrick Schüffel, Finanz-Professor im schweizerischen Freiburg, wird dieser Job zwischen 2023 und 2033 mit einer Wahrscheinlichkeit von 43 Prozent vom Computer übernommen. Ein Beispiel dafür, dass der digitale Kollege, der uns in den letzten Jahren mehr und Routinearbeit abgenommen hat, künftig auch intellektuelle Aufgaben übernimmt.

Schüffel stützt sich bei seiner Prognose auf eine Arbeit von Carl Benedikt Frey und Michael Osborne mit dem Titel “The Future of Employment”. Darin haben die beiden Wissenschaftler, gestützt auf offizielle Jobbeschreibungen der US-Regierung, 702 Berufe untersucht. Sie prüften mit einem mathematischen Modell, das auf Basis bisheriger Trends Prognosen erstellte, die Wahrscheinlichkeit des Verschwindens von Jobprofilen. Ihre Schlussfolgerungen sind dramatisch: “Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Das heißt, die entsprechenden Tätigkeiten können irgendwann in der Zukunft, vielleicht in zehn oder 20 Jahren, automatisiert werden.”

Schüffel hat gezielt die Daten für die Bankbranche für das Jahrzehnt bis 2033 aus der Studie herausgezogen. Die Ergebnisse zeigen eine große Bandbreite. So liegt die Wahrscheinlichkeit, dass Verkäufer im Wertpapierbereich überflüssig werden, bei nur 1,6 Prozent. Auf der anderen Seite sind “persönliche Finanzberater” mit 58 Prozent Risiko in hohem Maße bedroht. Noch schlimmer sieht es für Leute aus, die lediglich per Hand Daten erfassen: Mit 99 Prozent Risiko hat der Beruf kaum eine Überlebenschance. Dasselbe gilt aber mit 98 Prozent auch für Buchhalter und Kreditsachbearbeiter. Zum Teil enthält die Aufstellung allerdings kaum erklärbare Differenzen: Finanz-Analysten sind nur zu 23 Prozent bedroht, Kredit-Analysten dagegen zu 98 Prozent.

Das letzte Beispiel zeigt die Grenzen derartiger Prognosen. Letztlich handelt es sich um Gedankenspiele, bei denen der eigentliche Wert weniger in den Prozentzahlen liegt als darin, Denkanstöße zu geben. Ein wichtiger Punkt ist dabei: Arbeiten, die allein eine hohe abstrakte Intelligenz erfordern, gelten als durchaus ersetzbar. Je mehr hingegen soziale Intelligenz und Kreativität gefragt sind, desto weniger Chancen hat Kollege Computer. Daher sind Verkäufer schwer zu ersetzen, auch wenn sie vielleicht weniger abstrakte Intelligenz brauchen als Ökonomen.

Soziale Kompetenz als ein Ausweg Ausschlaggebend für die Einschätzung der jeweiligen Berufe ist daher, wie die damit verbundenden Aufgaben eingeschätzt und gewichtet werden. Besteht die Aufgabe des Ökonomen vor allem darin, eine Konjunkturprognose für das nächste Quartal abzugeben? Dann hat der Kollege Computer eine gute Chance, ihn abzulösen. Schon heute gibt es Unternehmen wie etwa Now-Cast, bei denen selbstlernende Software kurzfristige Prognosen übernimmt. Oder besteht die Aufgabe der Ökonomen eher darin, Daten zu erklären und Rahmenbedingungen für die wirtschaftliche Entwicklung zu analysieren? Da tut sich der Computer schon schwerer. Viele Bank-Ökonomen arbeiten zudem de facto in der Kundenbetreuung. Sie unterhalten sich mit Großkunden über ökonomische Fragen.

Das dient nicht nur dazu, harte Schlussfolgerungen, etwa für Investitionen, logisch abzuleiten. Anleger, die ihre Entscheidungen unter hoher Unsicherheit treffen müssen, suchen versierte Gesprächspartner, mit denen sie die Last dieser Unsicherheit teilen können. Bei dieser Aufgabe ist das persönliche Gespräch durch nichts zu ersetzen, nicht einmal durch Videokonferenzen, geschweige denn den Computer.

Das Beispiel zeigt, dass der Computer viele Berufe nicht ersetzt, sondern sie verändert und die Gewichte verschiebt. So gibt es etwa bei freien Finanzberatern in den USA den Trend, Anlage-Entscheidungen tatsächlich Computern, den sogenannten Robo-Advisern, zu überlassen. Kernaufgabe des Beraters ist dann nicht mehr, dem Kunden einen angeblich heißen Aktientipp zu geben. Vielmehr muss der Dienstleister helfen, eine Einschätzung seiner finanziellen Situation und Risikobereitschaft herzuleiten. Diese kann dann Grundlage für die maschinelle Verwaltung eines Depots werden.

Heute schon gibt es auch Firmen, die vom Handel an den Kapitalmärkten leben, ohne einen einzigen Händler zu beschäftigen. Die Aufträge werden vom Computer erledigt. Aber die jeweilige Software entsteht in Zusammenarbeit von Computer- und Kapitalmarktexperten. Für viele Banker dürfte gelten, was Frey und Osborne als Schlussfolgerung ziehen: “Damit Beschäftigte das Rennen gewinnen, müssen sie kreative und soziale Kompetenz erwerben.”

ZITATE FAKTEN MEINUNGEN

Nach unseren Schätzungen sind 47 Prozent der Stellen in den USA einem hohen Risiko ausgesetzt. Carl Benedikt Frey, Michael Osborne Professoren in Oxford

https://www.financial-career-bw.de/news-events/news/detailansicht/artikel/welche-bankjobs-der-computer-uumlbernimmt/

Increasingly often I am being asked by students, colleagues, investors, even friends and family “What is Fintech?”. I then typically answer “Fintech is an industry made up of organizations using novel financial technology to support or enable financial services”. And then, to avoid misunderstandings I add “A Fintech is an organization that uses novel financial technology to support or enable financial services”.

Increasingly often I am being asked by students, colleagues, investors, even friends and family “What is Fintech?”. I then typically answer “Fintech is an industry made up of organizations using novel financial technology to support or enable financial services”. And then, to avoid misunderstandings I add “A Fintech is an organization that uses novel financial technology to support or enable financial services”.

Yet, what sounds like a pretty straight-forward answer, was a hard nut to crack. In fact, the term Fintech is so often and widely used that some people even increasingly shun using it altogether.* To them the concept of Fintech has become too comprehensive and too ubiquitous to have any conclusive meaning any longer. For me it required quite a thought process to come up with a telling definition. This is due to several reasons.

First, a definition is never true or false per se, but more or less useful in a specific context. For instance, think about the term “power”. How would a physicist define it? How a politician? Which definition would a judge provide? Which explanation would an athlete give? Moreover, even within the domain of sports you are likely to receive different answers, depending on whom you ask. A weight lifter will most probably provide you with a different answer is than the fellow athlete from the same Olympic team who competes in synchronized swimming. Hence, we have to accept that – contingent on the counterparty you ask – one may well receive varying answers on the identical question. The same applies to the expression Fintech.

Looking at the most popular encyclopaedia of our times, Wikipedia, we can read that “[f]inancial technology, also known as fintech, is an economic industry composed of companies that use technology to make financial services more efficient.” (Wikipedia, 2016a). Conveniently enough for the reader, Wikipedia also provides us with the source for their definition. Wikipedia refers to the Wharton FinTech Club which provided this definition (Wharton Fintech, 2014). In a similar vein Susanne Chishti and Janos Barberis state in their landmark book on Fintechs that “Financial Technology or FinTech is one of the most promising industries in 2016” (Chishti & Barberis, 2016, p.5). The Oxford Dictionary tells us that Fintech is a mass noun (Oxford English Dictionary, 2016). More specifically this most authoritative source for British English suggests that Fintech are “Computer programs and other technology used to support or enable banking and financial services: fintech is one of the fastest-growing areas for venture capitalists”. In this context it may also be noteworthy that the most widely used dictionary and thesaurus for American English, Merriam-Webster, does not offer any definition for the term (Merriam-Webster, 2016).

On one popular Web sites in the Fintech sphere one can find the following definition “Fintech is a line of business based on using software to provide financial services.” (Fintech Weekly, 2016). Interestingly enough on that very Website reference is made to Wikipedia which – at least today – provides a different definition. On another blog from the finance world one can read a definition provided by Harry Wilson of Claro Partners: ”FinTech is an ecosystem of startups” (Wilson, 2015).

We could almost indefinitely continue this exercise of extracting definitions for the term Fintech from various authors. Yet, already from this very short although not representative selection of definitions, we can conclude that there is a vast range of meanings of the word Fintech: from “computer programs” and “other technologies” over “line of business” and “ecosystem” to an “industry”. This plethora of connotations makes it hard, if not impossible, to distil one commonly accepted explanation.

Interestingly enough even some of the biggest consultancies which certainly employ some of the smartest minds on the planet shy away from defining the term Fintech. Regularly one can find reports on Fintech related topics which do not provide any definition of the term Fintech itself; see for instance the McKinsey report on the effects of Fintech on banks by Dietz, Khanna, Olanrewaju & Rajgopal (2015) or the BCG report on the opportunities Fintech provides to corporate banks by Dany, Goyal, Schwarz, Berg, Scortecci & Baben (2016).

The second reason, why it is so inherently difficult to define the concept of Fintech is because definitions change over time. Also here we have some analogies. As an illustration think about the expression “information technology” (IT). In the early days of computing IT stood for items such punched tapes and cathode ray tubes. Today, however, we much rather associate things such as Motion User Interfaces, Bots and the Internet of Things with IT. Consequently, it is also safe to assume that the expression Fintech undergoes change. The definition provided by Investopedia pays tribute to this fact: “Fintech is a portmanteau of financial technology that describes an emerging financial services sector in the 21st century. Originally, the term applied to technology applied to the back-end of established consumer and trade financial institutions. Since the end of the first decade of the 21st century, the term has expanded to include any technological innovation in the financial sector, including innovations in financial literacy and education, retail banking, investment and even crypto-currencies like bitcoin.” So, for the authors of Investopedia, Fintech was originally an expression describing banking backend technology, but widened over time to also encompass technological innovations in financial services and related areas (Investopedia, 2016). Following the authors of Investopedia Fintech is not just a mere industry, but also a technology and an expression for innovation.

So far we have been talking about “Fintech” – without prefixed article. However, during conversations, but also in texts one also regularly encounters the expression “a Fintech”. Is there a difference between “Fintech” and “a Fintech”? If so, what is the difference? To my experience people typically refer to a Fintech company or more specifically to a Fintech start-up when they talk about “a Fintech”. Hence, the difference is the “level of analysis” as the scientist would say. As explained above “Fintech” without article typically relates to an entire a group of objects whereas “a Fintech” is just one single entity. This apparently small difference by the prefix “a”, can give rise to serious misunderstandings. To a politician, for instance, it will make a world of difference, whether he or she is asked to support creating an industry cluster or even entire industry or just one single firm. The same goes for a venture capitalist albeit with opposite signs.

Fourth and last, confusion about the term Fintech emerges from the fact that definitions can vary across languages. To illustrate this fact, I recommend to take a look at the various definitions of Fintech provided by different language versions of Wikipedia. The Italian site, for instance, states that Fintech is the “provision” of financial products and services using information technologies [“La tecnofinanza, o tecnologia finanziaria (in inglese Financial Technology o FinTech) è la fornitura di servizi e prodotti finanziari attraverso le più avanzate tecnologie dell’informazione (TIC)”] (Wikipedia, 2016b).

By contrast, the German Wikipedia definition of Fintech suggests that Fintech is an umbrella term for “modern technologies in the area of financial services” [“Finanztechnologie (auch verkürzt zu Fintech bzw. FinTech) ist ein Sammelbegriff für moderne Technologien im Bereich der Finanzdienstleistu ngen”] (Wikipedia, 2016c).

The French Wikipedia version is much closer to the English one, yet it does not define Fintech as an industry, but more loosely as an “area of activity” [“La technologie financière, ou FinTech, est un domaine d’activité dans lequel les entreprises utilisent les technologies de l’information et de la communication pour livrer des services financiers de façon plus efficace et moins couteuse”] (Wikipedia, 2016d).

Hence, just by comparing across languages one can already fathom the potential for misunderstandings. While the Frenchman may be talking about Fintech as a business segment, the German may be speaking about technologies, the Italian about a delivery channel and the native English speaker may refer to an entire industry. Being aware of potential pitfalls is all the more important as the term Fintech is derived from the English words Financial Technology and also used as such in various other languages. Thus people may automatically assume that they talk about identical things whilst they are not. In addition one should bear in mind that Fintech is a global phenomenon. Running into questions of semantics across languages may happen easier than anticipated.

However, we can live with this ambiguity in definitions. In fact we have been living with this ambiguity for years, if not decades, in other fields of business and academia. For example, think about the term “strategy”, “innovation” or “business model”. We use them on a daily basis, yet we have not established one common definition for any of them. Hence, having not one single definition for the word Fintech has not and should not prevent us from using it. However, when talking about Fintech we should make clear to our audience what we mean by Fintech. Providing a little explanation for our audience may therefore significantly improve the efficiency of communication and reduce the potential for misunderstandings. If you want to be extra polite you may also want to explain to your vis-à-vis why you use one specific definition and not another.

Once more I want to stress that none of the definitions provided above are right or wrong as such. Rather than that they are more or less useful in certain contexts. The definition I provided above, “Fintech is an industry made up of organizations using novel financial technology to support or enable financial services”, is very similar to the one provided by the Wharton Fintech Club and which is being promoted by the English Wikipedia site. Yet, I prefer to use the more broadly defined word organization instead of company. Companies are typically profit seeking and hierarchically organized. More and more often, however, we see non-hierarchical organizations such as The DAO to play a major role in the Fintech domain (The DAO, 2016). I purposely want to include these organizations in my definition. What is more, I tightened my definition in comparison to the Wharton definition by extending it for the word “novel”. I did this because otherwise the more comprehensive Wharton definition would also include just any incumbent bank running on Cobol-coded host systems as they are using this (admittedly ancient) technology to be more efficient. Lastly, I added the verb enable to my definition of Fintech as I am convinced that Fintech is not just about enhancing efficiency, but also more fundamentally about enablement. The distributed ledger rendered possible by Blockchain technology or micropayments made available through telecommunication systems are just examples for theses empowering technologies. Attention should be paid to the fact that innovation emanating from Fintech can be anything from purely complementary to highly disruptive. If the innovation is barely supporting an existing business model in financial services it is likely to be complementary, whereas it will receive the label disruptive if it jeopardizes existing business models.

I am well aware of the fact that the definition I use is far from perfect. For instance, it does not provide definitions for its components. Hence, one could rightly ask, “So what do you specifically mean by ’industry’ and what by ’novel’”? And how do you delineate ’industry’ from ’ecosystem’?”. Moreover I am certain that also the definition I use nowadays will change over time with the advancement of technology and the evolution of business. Last but not least, there are many terms up and coming that constitute for spin-offs of the overall Fintech theme. Among those are “InsurTech”, “WealthTech”, “RegTech”, just to name a few. Time will show how are they will be used.

Nicolas Steiner, one of the founding members of Level39 recently shared an anecdote about a meeting with a couple of French speaking experts from the telecommunication industry who asked him whether Fintech stood for “the end of technology”. The reasoning for that being that they believed that Fintech was short for the French expression “la fin de la technologie”. I hope by providing and spreading sense making definitions of Fintech we will encounter less and less of such misunderstandings in the future.

Spiros Margaris, who is often referred to as one of the Key Influencers of Fintech scene, once stated “Fintech will never disappear, only some fintech startups will disappear.” No matter which definition was used here, it is almost safe to say that this statement will come true.

*At this point greetings go out to Nasir Zubairi who is considered to be one of the big Fintech minds of Luxembourg

Chishti, S., & Barberis, J. (2016). The FinTech Book: The Financial Technology Handbook for Investors, Entrepreneurs and Visionaries. Chichester, UK: John Wiley & Sons Ltd

Dany, O., Goyal, R., Schwarz, J., Berg, P. v. d., Scortecci, A., & Baben, S. t. (2016). Fintechs may be corporate banks’ best “Frenemies”.

Dietz, M., Khanna, S., Olanrewaju, T., & Rajgopal, K. (2015). Cutting through the FinTech noise: Markers of success, imperatives for banks. In G. B. Practice (Ed.): McKinsey & Company,.

Fintech Weekly. (2016). Fintech Definition. Retrieved from https://www.fintechweekly.com/fintech-definition

Investopedia. (2016). Fintech. Retrieved from http://www.investopedia.com/terms/f/fintech.asp

Merriam-Webster. (2016). fintech.

Oxford English Dictionary. (2016). fintech. Retrieved from http://www.oxforddictionaries.com/definition/english/fintech

The DAO. (2016). Overview. Retrieved from https://daohub.org/about.html

Wharton Fintech. (2014). What is FinTech? Retrieved from https://medium.com/wharton-fintech/what-is-fintech-77d3d5a3e677#.kczb2jawk

Wikipedia. (2016a). Financial Technology. Retrieved from https://en.wikipedia.org/wiki/Financial_technology

Wikipedia. (2016b). Tecnofinanza. Retrieved from https://it.wikipedia.org/wiki/Tecnofinanza

Wikipedia. (2016c). Finanztechnologie. Retrieved from https://de.wikipedia.org/wiki/Finanztechnologie

Wikipedia. (2016d). Technologie financière. Retrieved from https://fr.wikipedia.org/wiki/Technologie_financi%C3%A8re

Wilson, H. (2015). The new shape of FinTech is making the world a better place. Retrieved from https://www.finextra.com/blogposting/11518/the-new-shape-of-fintech-is-making-the-world-a-better-place

Professor Dr. Patrick Schüffel

patrick.schueffel@hefr.ch

Haute école de gestion Fribourg

Institute of Finance

Chemin du Musée 4

CH-1700 Fribourg

[posted on LinkedIn on July 20th]

Why it could be worthwhile to look at the banking world over the rim of one’s tea-cup

Why it could be worthwhile to look at the banking world over the rim of one’s tea-cup

Most likely the music industry would have never dreamt of Apple becoming their biggest competitor. In a similar vein established mail order businesses had never imagined that the auction house Ebay and the book store Amazon would suddenly pull the rug from under their feet. And the camera manufacturers of this world carefully watched each other’s every move but obviously lost sight of the digital competition. For Kodak this ended deadly.

But how about today’s banks? What would happen if an industry outsider would enter the banking industry and would pose a serious competition for the established players? For instance, what would happen if Google would decide to setup a bank?

First of all it should be noted that the necessary cash is available. With approximately 60 billion US Dollar Google has a pile of cash at its disposal that is waiting to be assigned to a specified use. The entry hurdle cash is thus negligible. One could even go as far to say that Google could easily absorb a total write-off in case the banking venture should fail.

Moreover, cost advantages may arise through the technology leadership that Google possesses. Incumbent banks regularly struggle with IT legacy systems that had often been built in the eighties of the previous century. These core banking systems had not only been developed in programming languages which are hardly known these days any longer, but they are based on a process oriented approach which is antiquated given today’s object oriented program codes. Merely keeping those systems alive already eats up a fair share of the entire IT budget of many banks. Google would not have these legacy problems. Google could build a new bank based on the latest IT technology on a green field or – to be more precise – in a green cloud.

But does Google have the necessary reputation to do banking? Conventional wisdom has it that banks should be serious, conservative, maybe even a little bit outmoded. At first glance this notion does not sit well with a playful service provider whose corporate identity was coined by the colours of Lego bricks and that grew large in the Internet. At closer inspection, however, one can observe that already today clients entrust Google with almost any information. The trust in Google appears to be boundless as far was data is concerned. Why should that be different in money matters?

But what about Google’s potential clients? Who would entrust a Google Bank with his or her money? In this context it must be noted that as of today Google has already more than 400 million clients with user accounts that source various products and services from Google, from email accounts over translation or navigation services to hardware such as the Google tablet. The list is almost open-ended. If only a fraction of these clients would become clients of a Google Bank it would mean millions.

To put it at its simplest the business model of Google consists of collecting, condensing and editing data in a user-friendly fashion. Google has honed this model to perfection. Should Google now decide to offer banking services we could also expect to see this type of sophistication in banking. As an extreme case Google could for example scan the mail box of a client (as is already happening today). If there are any indications that the client may want to purchase a house, Google could proactively offer a mortgage to this client. Google has the potential to reveal client needs and to make corresponding offers even before the client is clear on his or her need himself or herself.

Last but not least Google has an outstanding reputation as an employer. When it comes to winning employees for a new Google Bank, Google could easily keep up with incumbent banks – at least as far as the under 35 year olds are concerned. As the banking industry’s neophyte Google could differentiate itself from the alleged causers of the financial crisis. It is safe to assume that Google could fight the war for talent from a vantage point.

If the preconditions are so favorable for Google why has Google then not long entered the banking industry? A plausible explanation could be that Google still considers the banking sector as too unattractive. But this could change soon as Google has already made first steps towards banking with the Google Wallet and by obtaining a license as an Electronic Money Institution. This leaves incumbent banks with two options in the meantime: one could be entering a partnership with Google and forming an alliance with the technology giant. The second option would be to swiftly whip finances into shape, to polish up the image of the bank, to increase the customer base, to improve client service and to enhance the relationship with the employees – quite simply to be geared to Google in these matters.

Hence, when looking at the own position in the banking industry, it could be worthwhile to get one’s bearings not solely by looking at the other competitors in the banking business. Looking at the banking world over the rim of one’s tea-cup could thus be a valuable exercise.

Note from the author:

This is the English translation of a German post that was published on the Swiss financial blog ‘Inside Paradeplatz’ on 04 March 2015. Due to numerous feedback on the German post, manifold requests of non-German speakers to translate the text, but also due to the fact that I attended some utmost inspiring presentations by Patrick Warnking and Sandra Emme of Google Switzerland in the meantime, I decided to also publish the English version of this post.

Dr. Patrick Schüffel, A.Dip.C., M.I.B., Dipl.-Kfm.

Adjunct Professsor

Haute école de gestion Fribourg

Chemin du Musée 4

CH-1700 Fribourg

patrick.schueffel@hefr.ch, www.heg-fr.ch

FinTech, a game-changing alloy of technology and finance, blends innovation-focused technology companies with traditional financial sector players. The merger of these two different business approaches, the tech and the traditional one, is the bedrock of the future financial sector landscape. Luxembourg, with its modern financial institutions, is well positioned to take reigns of the FinTech revolution.

With its vibrant ecosystem of financial institutions, technology companies, R&D centres, and a highly diversified and specialised economy, Luxembourg is an emerging FinTech innovation hub. “The country already provides factual support to innovation by encouraging private and public funding, and by building up a true start-up support ecosystem: the government put FinTech as one of the six key domains of the Digital Lëtzebuerg Strategy launched in 2014, aimed at turning Luxembourg into a digital nation, and mandated Jeremy Rifkin to examine and advise on how the Grand Duchy can leverage its FinTech potential” says Gregory Weber, FinTech Leader at PwC Luxembourg.

The Grand Duchy provides an attractive ecosystem not only for FinTech companies, but for business in general. Adding its innovative and responsive regulatory environment, Luxembourg is the epitome of a FinTech aware business environment. Local market players seem to perfectly understand that by embracing the FinTech business model, the Grand Duchy is on the right path to further strengthen its recognition and reputation among investors, clients and the start-up community.

“Internet, mobility, social networking and the rise of price comparison websites have changed the game over the past decade and have created a new generation of customers who demand simplicity, speed and convenience in their interactions with financial providers and even with their peers” highlights Gregory Weber. Traditional market players have started adapting to new market demands. The need to meet changing customer expectations with new offerings (resulting in an increased focus on the client experience) is top-of-mind for 86% of Luxembourg respondents when asked about the most important impact of FinTech on their business.

According to the survey, nearly all (94%) respondents from the traditional financial industry believe that part of their business is at risk of being lost to standalone FinTech companies. Incumbents believe that more than a fourth part (26%) of their business could be at risk due to further development of FinTech, though FinTech companies anticipate that they will be able to take over only 10% of incumbents’ business (compared to 33% globally). “In this regard, the asset & wealth management industry is feeling particular pressure from FinTech companies” adds Gregory Weber.

On the other hand, insurers in Luxembourg may be underestimating the threat posed by FinTech with an estimated share of business at risk of only 10%, compared to 21% for global insurance participants.

However, not only are traditional financial industry providers concerned about losing part of their business to FinTechs, they are also aware that their ways of working and product offerings will be challenged and possibly transformed.

Blockchain represents the next evolutionary jump in business process optimization technology. If blockchain gains wider acceptance, it could lead to significant changes in back-office roles, as ownership could be transferred without the need for intermediaries and reconciliations would disappear once there is a shared ledger that all parties agree on. “In Luxembourg, the majority of respondents (60%) recognises blockchain’s importance and is much more willing to respond to blockchain when compared to global respondents (except for asset & wealth managers). However, none of the respondents declares being extremely familiar with the technology. Only 17% believes being very familiar with it while one in five Luxembourg industry players is not familiar with blockchain at all” highlights Gregory Weber.

The ability to collaborate, at both a strategic and business level, with a few key partners could soon become a competitive advantage of Luxembourg financial industry.

Almost half (44%) of Luxembourg financial sector players believes that FinTech is integrated at the heart of their corporate strategies. However, more than 50% either does not have a fully aligned corporate FinTech strategy or FinTech does not have any role or impact within the strategic corporate agenda. There is no clear industry-wide trend in terms of how traditional players deal and engage with FinTechs. More than a third (34%) engages in joint partnerships with FinTech companies, 31% buys and sell services to FinTech companies, 14% rebrands purchased FinTech services (white-labelling), 14% launches their own FinTech subsidiaries, one in ten establishes start-up programs to incubate FinTech companies and 7% sets up venture funds to fund FinTech companies. Surprisingly, 21% of Luxembourg participants does not deal with FinTech at all. When both parties (traditional financial and FinTech companies) are asked about the biggest impediments when dealing with one another, incumbents name regulatory uncertainty (68%), IT security (45%) and differences in operational processes (45%). FinTechs, on the other hand, are mostly concerned about different management culture when dealing with incumbents (67% of respondents) and IT security (50%) is also a concern.

While the responses from Luxembourg participants are generally aligned with the global ones, the required financial investments for Luxembourg FinTechs when dealing with traditional financial companies (50%) clearly stand out. Globally, this issue is FinTechs’ smallest concern, raised only by 28% of survey participants.

“FinTech is re-shaping the financial sector at such a pace that those players that stay behind today might not even recognise the sector in five years. With their potential, Luxembourg players, however, have all the capabilities to stay at the heart of the FinTech revolution. The golden rule: start embracing FinTech now” concludes Gregory Weber.

Legend:Gregory Weber, FinTech Leader PwC Luxembourg – Nicolas Mackel, CEO Luxembourg for Finance – Jonathan Prince, Co-Founder Digicash Payments SA – Romain Godard, Partner PwC Strategy& – Patrick Schüffel, COO, Saxo Bank AG – Nasir Zubairi, Entrepreneur/Investor

Notes to Editors:

About the report :

The 2016 PwC Global FinTech Survey gathers the view of 544 respondents from 46 countries, principally Chief Executive Officers (CEOs), Heads of Innovation, Chief Information Officers (CIOs) and top management involved in digital and technological transformation, distributed among five regions.

The Luxembourg-focused cut was based on the responses of 36 respondents from the financial industry’s major market players.

For a copy of the report and to see the full results, please visit www.pwc.lu

Die Schweizer Banken sind noch Lichtjahre von Open-Innovation-Plattformen entfernt. Dabei liessen sich damit zu extrem tiefen Kosten extrem viele grossartige Ideen gewinnen, sagt der Ex-Credit-Suisse-Manager und heutige Finanzprofessor Patrick Schüffel.

Von Patrick Schüffel, Professor an der Hochschule für Wirtschaft Fribourg und Direktor des dortigen Instituts für Finanzen

McDonald’s tut es und BMW auch, Mammut, Coca-Cola und Bosch ebenso wie Procter & Gamble. Sogar Napolen Bonaparte tat es. Sie alle betreiben – oder im Falle Napoleons betrieben – Open Innovation.

McDonald’s lancierte in Deutschland die Aktion «Mein Burger», in der Kunden ihren eigenen Hamburger zustellen konnten. Der Outdoor-Bekleidungshersteller Mammut suchte auf der Open-Innovation-Plattform Atizo nach Ideen für einen neuen wetterfesten Reissverschluss.

Wie Napoleon die Konservendose erfand

Und Coca-Cola ist auf Facebook und mit einer «Happiness App» bei Millionen von Usern auf der Suche nach neuen Marketing Themen. Bei Bosch wird auf der firmeneigenen Open-Innovation-Website vor aller Welt diskutiert, ob man nicht Plastikventilatoren statt Metallventilatoren in Autobauteilen nutzen sollte.

Die Firma Procter & Gamble bediente sich der Experten-Plattform Innocentive, um ihr Multi-Millionen-Dollar-Produkt «Spin Brush» zu kreieren. Und Napoleon schliesslich, schrieb einen Wettbewerb aus, in dem die besten Ideen eingereicht werden sollten, wie man Lebensmittel für seine Truppen besser haltbar zu machen. Ihm verdanken wir die Konservendose.

Die Geschwindigkeit der Ideen

So unterschiedlich die zu Grunde liegenden Fragestellungen auch sein mögen, die Motivation, sich des Open-Innovation-Ansatzes zu bedienen, ist immer identisch: Warum nur ein paar wenige Köpfe auf wichtige Fragestellungen ansetzen, wenn sich ebenso Dutzende, Tausende, ja sogar Millionen mit dieser Fragestellung auseinander setzen könnten.

Dabei besteht der Vorteil dieser Methode nicht nur in der schieren Anzahl von Ideen, welche Firmen damit einsammeln können. Die Geschwindigkeit, mit der Ideen unterbreitet werden, ist ebenfalls höher und der «Fit» der Ideen ist mitunter extrem gross, wenn es sich bei den Ideengebern ebenso um Kunden handelt.

Was machen die Schweizer Banken?

Das Beste dabei ist: Die Kosten, die der Open-Innovation-Ansatz verursacht, sind vergleichsweise gering. Dies ist sicherlich ein Faktor, der gerade in der heutigen Zeit nicht zu vernachlässigen ist.

Und was machen die Schweizer Banken? Fehlanzeige in Sachen Open Innovation. Oder um präzise zu sein, abgesehen von ein paar spärlichen Ausnahmen – Fehlanzeige.

Lichtjahre davon entfernt

Zwar haben die einen oder anderen Schweizer Banken schon die eine oder andere Frage auf der Open-Innovation-Plattform Atizo zur Diskussion gebracht, beispielsweise einen neuen Marketing-Claim. Aber mit diesem punktuellen Einsatz von Open Innovation sind sie noch Lichtjahre davon entfernt, dieses Konzept als festen Bestandteil ihrer Unternehmensprozesse zu betrachten.

Dabei gibt es durchaus Beispiele, wie es gehen könnte. Die Commenwealth Bank of Australia etwa macht mit ihrer «Idea Bank» (Bilder oben) vor, wie man kontinuierlich auch im Bankgeschäft Open Innovation betreiben kann. Seit etlichen Jahren vergibt sie jedes Quartal 10’000 australische Dollar für die beste Idee, die ihr unterbreitet wird.

Banking für das 21. Jahrhundert

Barclays in Grossbritannien hat mit der Website «We’re listening» eine Stelle geschaffen, wo Kunden der Bank ihre Ideen mitteilen können. Unsere österreichischen Nachbarn wiederum haben bei der Sparkasse das S-Lab erschaffen, wo regelmässig Aufrufe an Kunden ergehen, sich mit bestimmten Problemstellungen zu befassen.

Die Avanza Bank in Schweden hat die Internet Initiative «Labs» gestartet, in der wiederum jeder Kunde jegliche Ideen eingeben kann. Auch die russische Sberbank hat mit «Sberbank 21» eine Open-Innovation-Initiative auf den Weg gebracht, um Ideen für das Banking des 21. Jahrhunderts einzusammeln.

Unmengen neuer Ideen

Was ist also los, warum hat Open Innovation nicht schon längst auch in der Schweizer Bankenbranche Einzug gehalten? Die Vorteile liegen doch auf der Hand: Unter vergleichsweise extrem geringen Kosten könnten extrem schnell Unmengen neuer Ideen für das Schweizer Banking generiert werden.

Liegt es eventuell daran, dass wir uns generell mit Neuerungen schwer tun und erst recht mit solch weitreichenden Neuerungen wie Open Innovation?

Leiden an einem Syndrom?

Liegt es an der Kultur der Schweizer Banken, die vielleicht immer noch unter dem «Not invented here»-Syndrom leiden und jeglicher Idee, die von aussen auf die Firma zugetragen wird, misstrauisch gegenüber steht?

Liegt es möglicherweise an einem Hierarchiedenken, das es allenfalls nicht zulässt, dass eventuell ein Kunde eine (bessere) Idee hat, die der Produktexperten der Bank nicht hatte?

Zunächst vielleicht ein Widerspruch

Möglich. Aber all diese Gründe sind es kaum wert, es nicht doch einmal mit Open Innovation zu probieren. Zudem könnte man ja zunächst einmal klein anfangen und Open Innovation innerhalb der Firma praktizieren, auch wenn dies zunächst einmal wie ein Widerspruch in sich aussehen würde.

Warum nicht fachspezifische Fragestellungen einem grösseren Publikum öffnen? Warum nicht eine firmeninterne Website bereitstellen, auf welcher der Kundenberater mit den Experten von Strukturierten Produkten darüber diskutieren kann, ob und wie Hypotheken gegebenenfalls mit solchen Finanzinstrumenten ergänzt werden könnten.

Fast nichts zu verlieren

Warum nicht alle Mitarbeiter befragen, wie mehr Kreditkartenpakete abgesetzt werden könnten. Warum nicht sämtliche Personalkunden – falls Interesse besteht – miteinbeziehen, wenn es darum geht, neue Self-guided Internet-Angebote zu erstellen?

Die Möglichkeiten, die sich den Banken mit Open Innovation bieten, stellen ein ungeahntes Potential dar, das noch nicht einmal ansatzweise abgerufen wurde. Es gibt mit diesem Ansatz fast nichts zu verlieren, aber mit Nicht-Einsatz von Open Innovation eine Menge zu verlieren – im schlimmsten Fall die Wettbewerbsfähigkeit.