Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Avec son numéro d’avril 2017, le journal suisse «Bilan» a récemment publié un supplément sur Fintech en Suisse. J’étais ravi de constater que l’éditeur a cité ma définition de Fintech, précédemment publiée dans le Journal of Innovation Management. Comme la publication originale était en anglais, la traduction française publiée par Bilan est la suivante:

«Fintech est une nouvelle industrie financière qui déploie la technologie pour améliorer les activités financières.»

(Patrick Schueffel tel que cité par Comment la suisse se profile comme un centre Fintech compétitif, Bilan 4/2017, supplément Fintech – Construire la finance de demain, p.6)

“Fintech is a new financial industry that applies technology to improve financial activities”(Schueffel, 2016; p. 45)

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg, Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Nach der Durchsicht von über 200 wissenschaftlichen Artikeln, die im Verlaufe der vergangenen 40 Jahre erschienen und in welchen das Wort Fintech benutzt wurde, hatte ich in diesem Artikel die folgende Definition des Begriffs Fintech abgeleitet:

“Fintech is a new financial industry that applies technology to improve financial activities” (Schueffel, 2016; p. 45)

Da der Artikel ausschließlich auf Englisch veröffentlicht wurde, erreichten mich zwischenzeitlich zahlreiche Anfragen, wie diese Definition ins Deutsche zu übersetzen sei. Gerne möchte ich diese Frage mit der folgenden deutschen Definition beantworten:

„Fintech ist eine neue Finanzindustrie, welche Technologie verwendet, um finanzielle Aktivitäten zu verbessern.“

Mit besten Grüssen

Patrick Schüffel

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion Fribourg

Chemin du Musée 4

CH-1700 Fribourg

patrick.schueffel@hefr.ch www.heg-fr.ch

“Fintech is a new financial industry that applies technology to improve financial activities.” (Schueffel, 2016; p. 45)

This is the definition I derived after examining more than 200 scholarly articles that were published over a period of 40 years and which are referencing the word Fintech in one way or the other. Building on the commonalities of the definitions that found entry into those peer-reviewed journals I distilled the definition provided above.

I am proud that my work withstood the rigorous double-blind peer review process of the Journal of Innovation Management and was published these days.

As the Journal of Innovation Management is an open access journal you can retrieve the full text by using the following link:

Schueffel, P. (2016). Taming the Beast: A Scientific Definition of Fintech. Journal of Innovation Management, 4(4), 32-54.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.

Have you even tried to explain the Blockchain concept to a seasoned private banker? Have you tried to describe the notion of a distributed ledger to this type of auditorium? And have you experienced the same result as I have over and over again: have you, too, just banged your head against a brick wall? I pondered the question why it was so much harder to explicate the concept to alleged banking experts than to first-year business students.

Use the right vocabulary

After numerous futile explanation attempts, it dawned on me. I was using the wrong vocabulary. Using the word ledger is counterproductive to the cause. When talking about a ledger, the traditional banker immediately translates that term into “bankbook” and that is the book in which the bank keeps all records of all customers adding and taking money from their bank accounts. It is thus the holy grail of private banking. Distributing the holy grail is inconceivable to many a private banker.

At that point it then hardly matters if you continue to explain that the users of the Blockchain are typically anonymized. It is almost futile to further explicate that, for instance, Bitcoin accounts are not tied to the identity of users and that anyone can create new and completely random Bitcoin accounts at any time, without the need to submit any personal information to any party. You have lost them already. Hence, what I found helpful in this situation is to refrain from using the term “ledger” altogether. Instead I call it distributed data base or distributed accounting system.

Give them a hands-on example

A friend of mine and design thinking pioneer, Michael Lewrick recently recommended me to do a hands-on exercise in particularly tough cases. Individually assign a random yet different number to every one of the ten bankers that are sitting in a room with you and have each of them note down their number and favourite colour on a separate sheet of paper. Have them pass on the paper to another participant and everyone repeats the exercise. Do so altogether ten times. In the end, everyone holds a list of 10 numbers and favourite colours in their hands. At this stage you can ask a) “What is Bob’s favourite colour?” – the others shouldn’t be able to tell as Bob’s identity has been anonymized. Yet you can also ask Bob, whether the correct colour is listed on his sheet – which should clearly be the case. And b) you can ask someone to now commit a “fraud”, i.e. to change the favourite colour of one participant – which should be nearly impossible unless the tasked fraudster does so on ten sheets of paper with the nine remaining group members agreeing. This exercise nicely explains some of the key features of the Blockchain and monies based thereon.

It’s worth trying

These two measures combined, using audience specific language and a hands-on exercise should therefore do the job. It certainly deserves a try. The Blockchain concept is too important as we could afford leaving private bankers behind. Happy explaining!

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

The number and diversity of Fintech offerings is soaring. As banking clients increasingly often enjoy not only a better user experience, but also cheaper rates at Fintech firms, their willingness to be locked-in with one or two universal banks diminishes. Henceforth clients will gradually assemble their own individual “banks”, comprising a range of offerings from different Fintech companies. Those firms which will be able to provide an overarching structure to seamlessly wrap the multitude of Fintech offerings will experience their heydays.

Modern production technology allows what would have been inconceivable only a few decades ago. If we want, we can have products of mass production tailored to our needs nowadays. Dell made only the beginning when first assembling PCs to our requests on a large scale. Today we order our tailored sneakers at Nike ID, wear a unique t-shirt from Spreadshirt and eat M&M’s sporting our very own initials. Yet, the trend of mass customization did not stop in the manufacturing sector. We can already observe its ramifications in the financial services industry where Robo-Advisors offer retail customers to tailor their client portfolios. But this is not the end point of the evolution. It is the mere beginning which will eventually lead to tailored banks.

The personal balance sheet

Like it or not, every single one of us carries his or her own very personal balance sheet: On the asset side, we have liquid asset positions such as the cash that we have in our wallets, the money on our current accounts, our savings accounts or money market instruments. Our personal investments may comprise medium term notes, bonds, stocks, mutual funds, pension savings and/or alternative Investments. Finally, we may possess highly illiquid real estate investments such as our primary residences, vacation homes or even property that we rent out.

On the liability side we may also have a variety of items. Current liabilities may include unpaid bills, credit card balances, taxes due, installment loans due in the short run, consumer loans, car loans, student loans, mortgages due within one year etc. Non-current liabilities may include any consumer, car or student loan that is due after one year. Last but not least, we may have mortgage debt for our primary residence and/or vacation homes and/or rental property.

Hence, as individual as we are as human beings, as individual are our personal balance sheets. Yet, what we do have in common is that we willingly or unwillingly manage these balance sheets. We carry out treasury functions on our personal balance sheets by paying bills and installments, transferring money from one account to another, by investing in shares or by redeeming mutual funds etc.

The Fintech Alternative

So far many consumers in the western world have ties to one or two banks, oftentimes universal banks, that cater to all of the needs resulting from these treasury transactions. Yet, the service offerings of universal banks are increasingly rivaled by Fintech firms that offer a narrow, yet highly specialized service or product.

If you have a little cash to spare, Fintech firms such as Creditgate24, LendingClub or Crowdcube, have offerings for optimizing liquid assets. To manage longer term investments one can turn to providers such Wealthfront, Moneyfarm, Nutmeg, Addepar etc. On the liability side, too, there is a vast array of Fintech companies jockeying for position. Current and medium term liabilities may be optimized by using Affirm, Borro, Lendable, Prosper etc.

In order to transfer money from one provider or account to another the consumer can chose among dozens of payment providers such as TransferWise, LiquidPay, Paypal and the likes. For trading purposes the client may want to turn to eToro or Robinhood. Even donating money becomes easier and less burdensome with Fintech providers such as Elefunds.

These new type of financial services providers that found their niches on specific links of the value chains of universal banks typically not only promise their clients a better user experience, but also lower costs. What is thus foreseeable for the near future is that clients will no longer accept to be locked-in with one or two banks, but that they will make use of a range of financial service providers. Eventually every user will assemble his or her very own bank, the IBank* as I call it.

Assembling the IBank

The IBank will comprise a selection of services provided by specific Fintech companies handpicked by the individual client. This can happen dynamically and on an ad-hoc basis or on a more permanent base. The client – or an overlaying algorithm for that matter – may decide on a case-by-case basis which payment service would be optimal for a specific transfer. On a more longer term basis one mortgage provider may be chosen until the renewal of the mortgage is due.

What is important to note, however, is that clients will make use of tailored “banks” which may be as personal as their individual balance sheet. The challenge and opportunity in this future banking world will be to provide the glue that seamlessly keeps together these services provided by different providers. Those providers who manage to assemble and maintain an overarching structure that smoothly integrates the multitude of service offering of Fintech providers will have a bright future in finance services world which is being ever more atomized.

*IBank like “I bank” – not to be mistaken with the iBank offerings by Barclays, The Bank of Georgia, Fransabank, BCU and so on.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

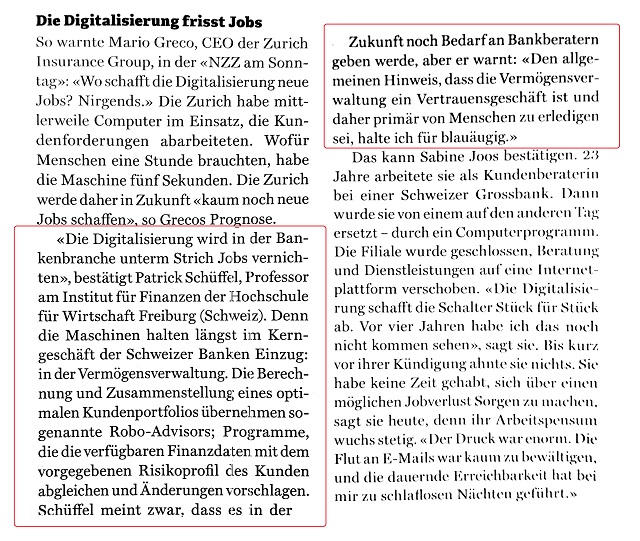

Jobangst, Digitalisierung, politische Umwälzungen: Das abgelaufene Jahr war heftig. Die Erschöpfung ist gross – auch bei Topmanagern. Was ihnen zu schaffen macht und wo sie Hilfe finden.

In 1984, one year before the sci-fi classic “Back to the Future” was released, the professors Danny Miller and Peter Friesen from McGill University in Montreal published a seminal paper on corporate life cycles. Both works contained clairvoyant features for the future.

Building on an empirical sample of firms the paper titled “A longitudinal study of the corporate life cycle” describes how companies can be classified into five life cycles from birth to decline. The authors applied five dimensions to accomplish this task: strategy, structure, environment and decision making style.

Fast forward 30 years. The year 2015 which was vividly described in “Back to the Future Part II” has just passed and an entire economic sector, namely the banking industry, appears to be in the doldrums. Many banks seem to be in decline.

Do you work for a bank in decline? Let’s have a quick lock how Miller and Friesen verbatim characterized a declining firm along the four dimensions thirty years ago (emphasis added):

1. Strategy

“Firms in the decline stage react to adversity in their markets by becoming stagnant […]. Firms seem to be caught in something of a vicious circle. Their sales are poor because their product lines are unappealing. This reduces profits and makes for scarcer financial resources, which in turn cause any significant product line changes to seem too expensive. So product lines become still more outdated […]; the firms just muddle through.”

2. Situation

“[…] There is a tendency to attend to what the owners want, that is, to preserve resources, rather than cater to the needs of customers. The market scope of declining firms is quite narrow […]. Failure in one major product line simply cannot be counterbalanced by success in others as might happen in more diversified companies […]. Shrinking markets can be extremely competitive and firms that rely totally upon them may find themselves in deep trouble. Performance thus tends to be very poor. This may be caused partly by the simple structure.”

3. Structure

“The locus of decision-making power is at the top of the firm. In fact, even routine operating decisions (these predominate in declining firms which shy away from strategic decisions) are executed by higher level managers […]. While managers who are close to customers and markets may be well aware of the problems that exist, their information does not seem to filter up to those with enough authority to do anything about it.”

4. Decision-making Style

“Decision making is characterized by extreme conservatism. There is little innovation, an abhorrence of risk taking, and a reluctance even to imitate competitors’ innovations, let alone lead the way […]. Sometimes it is due to the temperament of the top managers. Occasionally, it results from funds shortages stemming from previous declines in performance. But almost inevitably, key contributing factors are ignorance of markets […]. Managers fail to delegate and there is little in the way of participative management. Thus the top executives must spend most of their time handling crises. They just haven’t the time for much analysis. So they take very few dimensions into account in decision making […] and employ very short time horizons.”

Resonating with today’s banking industry

This rich description of a declining firm crafted in the year 1985 may resonate with many people across the globe working for banks in the year 2016. If it rings a bell with you, your bank may well be in decline. However, not all hope is lost: in their empirical study Miller and Friesen also showed that 42% of the firms in the decline phase progressed to the revival phase. But don’t get your hopes up too soon: Miller and Friesen describe the survivor bias as one of the major shortcomings of their study. Their empirical study only contained surviving firms. Those which did not make it through the decline phase were not included in their research.

Unfortunately, it appears as if Miller and Friesen’s 1984 description of declining firms had quite some clairvoyant features for many a bank of the year 2016.

Source:

Miller, D., & Friesen, P. H. (1984). A longitudinal study of the corporate life cycle. Management Science, 30(10), 1161-1183.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch,www.heg-fr.ch

Bundling will be the next big Fintech topic after unbundling and platformization. Just as consumers got used to buying different food items at one single supermarket long time ago, they will expect one-stop-shops for financial services. Those “bundlers” that manage to seamlessly offer cost-efficient and dynamic bundles are well poised for success in this next race in the Fintech arena. Some important lessons can be learned from previous bundling attempts, such as Deutsche Bank’s “Moneyshelf”.

In 2002 Deutsche Bank started an immensely ambitious e-commerce project. The objective of the project by the name of „Moneyshelf“ was to establish a financial super market. The goal was to create a one stop shop for virtually any financial product a retail client could wish for – across any provider existing. The underlying idea was to provide off the shelf financial products from any makers and brands. The reasoning behind it was that consumers would also frequent supermarkets to conveniently buy various products across brands and manufacturers. A modern consumer would visit a single supermarket to purchase bread, sausages, apples, beverages, canned food and cleaning liquid. He or she would no longer go through the ordeal of visiting a bakery to buy bread, a butcher to shop for sausages, a local market to get some apples and then drop by yet another store to buy beverages and food before visiting the local drug store to buy cleaning liquid.

Creating a financial supermarket

In order to use such a financial supermarket the client was requested to deposit his access information to any other banking service with the Moneyshelf platform. Moneyshelf would then let the client consolidate and manage all of his or her accounts in one highly user-friendly frontend. In the background online banking interfaces programmed by Deutsche Bank developers would ensure the interoperability. Moneyshelf promised a quantum leap in transparency and price efficiency. A client who would have a securities account with bank A and be invested in mutual funds from fund provider B could then not only shop for a more cost-efficient securities account, but also a better performing and less costly mutual fund und would only be a mouse click away. All of this was paired with features such as personal financial planners which offered insights on the clients’ spending and financial behavior and a rich offering of financial information and possibilities of analysis.

Deutsche Bank ahead of times

Moneyshelf as it was envisioned by Deutsche Bank was offering the client a tremendously versatile platform to choose among a vast range of providers and products such as current and savings accounts, mutual funds, brokerage services, mortgages, even life insurances. Deutsche Bank sensed that clients would become more tech savvy and consider the threat to be very real that Deutsche Bank may soon be disintermediated as far as their retail segment was concerned. With the emergence of online brokers and their strong growth Deutsche Bank feared of getting skinned and decided to take the bull by the horns. Hence, should a client decide to do business with a different bank, then Deutsche Bank would make sure that it would at least get a share of those revenue streams bypassing them.

The bone of contention: depositing client data

In the end this business model failed big time. The other banks, especially the rather dominant German savings banks warned their clients that it would be a violation of their contractual obligations to deposit account access information with any third party, including Moneyshelf. The savings banks maintained that they would not only refuse any liability in case of fraud, but that they would reserve the right to cancel the banking relationship with the client altogether should he or she access the account via Moneyshelf. Moreover the marketing campaign for Moneyshelf which depicted procreating animals was not very appealing to a largely conservative German retail banking segment.

Bundling as the central value propostion

Yet, Deutsche Bank got something right: the topic of bundling. As much as Fintech is about unbundling of banking services, a convenience loving customer does not want to sign up with Fintech Firm A to buy DJI stocks, with Fintech company B to convert some FX and with Fintech enterprise C to set up a financial plan. The levels of user experience and thus user expectations have never been higher than today. Hence, the emancipated banking client of nowadays would expect all of these services offered by one single provider and being accessible via one user interface (UI). Banking platforms such as N26, Moven, Bankin’ and Simple prove that the theme of bundling is highly topical as they oftentimes put together the services of a range of Fintech firms and offer them seamlessly through one UI.

The sophisticated future of bundling

However, the future of bundling will be much more sophisticated than that. Clients will expect not only expect cost-efficient but dynamic bundles. For instance, whereas payment provider A may be ideal for one money transfer from country X to country Y, it maybe payment provider B for the next transaction. Clients will not care which contractual obligations the platform is tied to, but the customer will expect the most cost-efficient Fintech firm to take over the task at hand. The same goes for stock brokerage or financial planning. The client will rightly demand to execute via the most cost-efficient broker and to set-up the financial plan with that one Fintech firm he or she sees most suitable. It will be the task of the platform owner or “bundle”, to tap into the Fintech eco-system to always find the most suitable service provider. The bundler must to put together these services for the consumer seamlessly and in a highly transparent fashion.

The race for bundling is on

The race for the best bundler will be open to Fintech firms and incumbent banks alike. This time, however, banks will no longer have a head-start for two reasons: first, a range of highly professional financial data aggregators such as eWise exist nowadays which can provide the necessary services off-the-shelf. Secondly an overhaul of EU legislation will update the rights and responsibilities of account information service providers, permitting intermediaries to obtain the account access information from clients. This change in legislation will come into effect in 2018 and it will be the starter’s gun for a European bundlers’ race in financial services.

Dr. Patrick Schüffel, Professsor, Institute of Finance, Haute école de gestion, Fribourg Chemin du Musée 4, CH-1700 Fribourg, patrick.schueffel@hefr.ch, www.heg-fr.ch

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.

Seasoned private bankers often do not grasp the idea of the Blockchain. It was not until I understood that I was using the wrong vocabulary that I could convey what the Blockchain was all about.